United States Active Pharmaceutical Ingredients Market Size and Forecast 2025–2033

U.S. API Market Expansion Accelerates on Strong Drug Demand and Biopharma Innovation

United States Active Pharmaceutical Ingredients Market Outlook

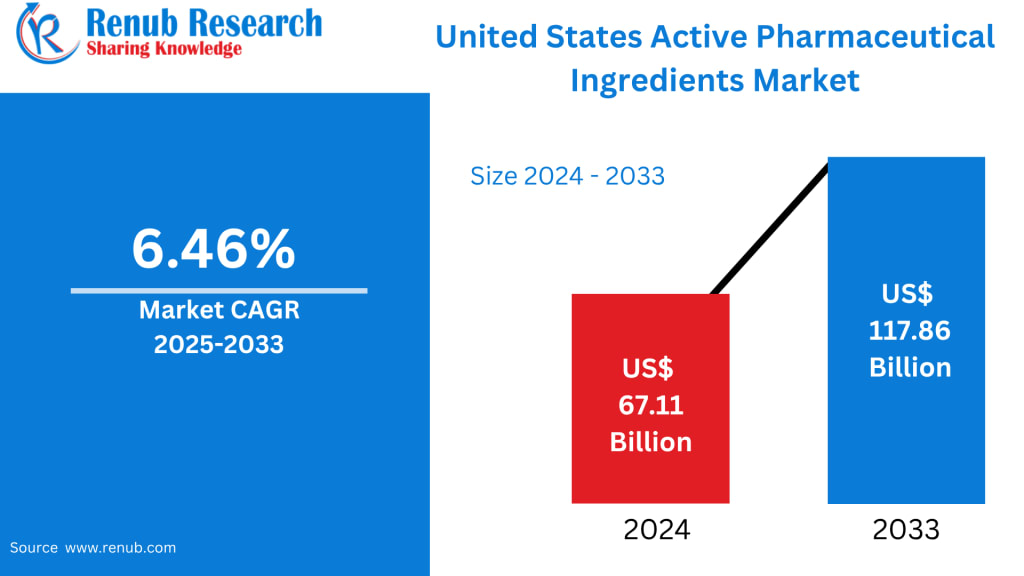

The United States Active Pharmaceutical Ingredients (API) Market is poised for sustained expansion over the coming decade, driven by robust pharmaceutical demand, innovation-led drug development, and a strong regulatory ecosystem. According to Renub Research, the market is expected to grow from US$ 67.11 billion in 2024 to US$ 117.86 billion by 2033, registering a CAGR of 6.46% during 2025–2033.

APIs form the foundation of modern medicines, providing the therapeutic action in both branded and generic drugs. In the U.S.—the world’s largest pharmaceutical market—APIs are central to drug innovation, chronic disease management, biologics development, and healthcare resilience. Rising healthcare expenditure, increasing disease prevalence, and strategic investments in domestic pharmaceutical manufacturing are collectively reshaping the U.S. API landscape.

United States Active Pharmaceutical Ingredients Market Overview

Active Pharmaceutical Ingredients are the biologically active components responsible for the intended therapeutic effect of medications. APIs can be derived through chemical synthesis, biotechnology, or fermentation, and are later combined with excipients to create finished dosage forms such as tablets, injectables, and capsules.

In the United States, APIs are indispensable to the production of prescription drugs, over-the-counter medicines, biologics, and specialty therapeutics. The country’s pharmaceutical ecosystem is highly advanced, supported by world-class research institutions, cutting-edge manufacturing facilities, and stringent regulatory oversight by the U.S. Food and Drug Administration (FDA). This framework ensures product safety, efficacy, and quality while encouraging continuous innovation.

Key Growth Drivers in the United States API Market

Rising Prevalence of Chronic Diseases

The increasing incidence of chronic conditions such as diabetes, cardiovascular diseases, cancer, and neurological disorders continues to fuel API demand across the United States. Chronic, non-communicable diseases account for the majority of healthcare utilization and pharmaceutical consumption nationwide. Long-term disease management requires continuous medication usage, significantly boosting the need for reliable, high-quality APIs.

An aging population, sedentary lifestyles, dietary changes, and rising obesity rates further exacerbate chronic disease prevalence. Pharmaceutical companies are responding by increasing R&D investments and expanding API production to support innovative and long-duration therapies.

Expansion of the Generic Drug Market

The expiration of patents for several blockbuster drugs has unlocked major opportunities for generic drug manufacturers. Generic medicines rely on the same APIs as branded counterparts but are sold at substantially lower costs, improving affordability and patient access.

The FDA’s push to accelerate generic and biosimilar approvals has strengthened the demand for cost-efficient, regulatory-compliant APIs. As healthcare systems and insurers increasingly favor generics to control costs, API suppliers serving the generic segment are experiencing strong, sustained growth.

Technological Advancements in Biotech APIs

Biotechnology is transforming the U.S. API market. Unlike traditional chemical APIs, biotech APIs—produced using recombinant DNA technology, cell culture, and fermentation—enable targeted therapies with improved efficacy and reduced side effects.

The growing success of biologics in oncology, immunology, and rare disease treatment has driven pharmaceutical companies to invest heavily in biotech API manufacturing facilities. Advanced platforms and process optimization technologies are improving scalability and production efficiency, making biologics a critical pillar of the future U.S. API market.

Challenges Facing the U.S. API Market

Supply Chain Dependence and Import Reliance

Despite its pharmaceutical leadership, the United States remains partially dependent on API imports, particularly from Asia. This reliance exposes the market to risks such as geopolitical tensions, pandemics, logistics disruptions, and raw material shortages.

Supply chain instability can lead to production delays and drug shortages, prompting policymakers and industry leaders to emphasize domestic API manufacturing. While reshoring initiatives are gaining traction, achieving full supply chain resilience remains a long-term challenge.

Stringent Regulatory and Compliance Requirements

The U.S. FDA enforces rigorous Good Manufacturing Practices (GMP) standards for API production. While these regulations ensure patient safety and product integrity, they increase operational costs and compliance burdens.

Smaller API manufacturers often struggle with the financial and technical requirements of frequent audits, documentation, and facility upgrades. As a result, regulatory compliance can act as a barrier to entry, limiting competition in certain API segments.

Market Segmentation Analysis

By Business Model

Captive APIs:

Captive API manufacturing involves pharmaceutical companies producing APIs internally for their own formulations. Large U.S. pharma firms favor this model to ensure quality control, protect intellectual property, and reduce dependency on external suppliers. Captive production enhances supply security and aligns API development closely with drug pipelines.

Merchant APIs:

Merchant API manufacturers supply APIs to third-party pharmaceutical companies. This model is vital for small and mid-sized drug developers lacking in-house manufacturing capabilities. Contract Development and Manufacturing Organizations (CDMOs) play a key role in scaling production and providing technical expertise.

By Synthesis Type

Biotech APIs:

Biotech APIs are witnessing rapid growth due to rising biologics approvals and strong pipelines in oncology and immunology. Government support, advanced research infrastructure, and accelerated regulatory pathways continue to strengthen this segment.

Synthetic APIs:

Synthetic APIs remain dominant in traditional therapeutic areas such as cardiovascular, CNS, and infectious diseases. Their cost-effectiveness, scalability, and established manufacturing processes ensure continued relevance despite growing biologics competition.

By Drug Type

Generic APIs:

The growing emphasis on affordable healthcare is driving strong demand for generic APIs. Manufacturers focusing on efficiency, sustainability, and regulatory compliance are gaining competitive advantage.

Innovative APIs:

Innovative APIs support novel drugs and specialty therapies. These APIs often involve complex synthesis, high potency, and stringent safety protocols, commanding premium pricing and margins.

Therapeutic Area Insights

Cardiovascular APIs

Cardiovascular diseases remain a leading cause of mortality in the United States. APIs used in antihypertensives, anticoagulants, and cholesterol-lowering drugs see consistent demand, supported by aging demographics and lifestyle-related health risks.

Oncology APIs

Oncology represents one of the fastest-growing API segments. High-potency APIs (HPAPIs) are critical for targeted cancer therapies, immuno-oncology drugs, and precision medicine. Strong R&D pipelines and unmet clinical needs ensure long-term growth.

Orthopedic APIs

Orthopedic APIs used in pain management, arthritis treatment, and bone health are gaining traction due to increasing obesity, aging populations, and musculoskeletal disorders.

Nephrology APIs

The rising prevalence of chronic kidney disease and end-stage renal disease is driving demand for APIs used in dialysis support, anemia management, and renal-specific therapeutics.

State-Level Market Dynamics

Key states driving API demand and manufacturing activity include California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, Washington, and New Jersey. These states benefit from strong pharmaceutical clusters, skilled workforces, and advanced healthcare infrastructure.

Competitive Landscape and Key Players

The U.S. API market is highly competitive, featuring global pharmaceutical giants and specialized API manufacturers. Each company is analyzed based on overviews, leadership, recent developments, SWOT analysis, and revenue performance.

Major companies operating in the market include:

Pfizer Inc.

Novartis AG

BASF SE

Teva Pharmaceutical Industries Ltd

Viatris Inc.

Sanofi Inc.

Merck KGaA

Dr. Reddy's Laboratories Ltd

Lupin Ltd

Bristol-Myers Squibb

Final Thoughts

The United States Active Pharmaceutical Ingredients Market is entering a decisive growth phase, underpinned by chronic disease prevalence, generic drug expansion, and rapid biopharmaceutical innovation. While challenges such as supply chain dependence and regulatory complexity persist, increasing investments in domestic manufacturing and advanced technologies are strengthening market resilience.

With strong demand across therapeutic areas and continued regulatory support for quality and innovation, the U.S. API market is well-positioned to remain a global leader through 2033—playing a critical role in shaping the future of healthcare, drug accessibility, and pharmaceutical sustainability.

About the Creator

Janine Root

Janine Root is a skilled content writer with a passion for creating engaging, informative, and SEO-optimized content. She excels in crafting compelling narratives that resonate with audiences and drive results.

Keep reading

More stories from Janine Root and writers in Longevity and other communities.

United States Pharmaceutical Market Size and Forecast 2025–2033

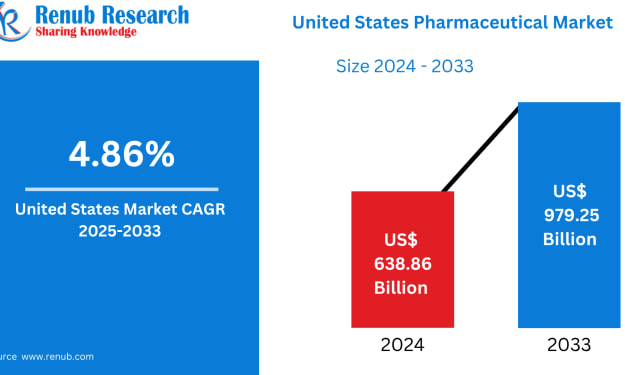

United States Pharmaceutical Market Outlook The United States Pharmaceutical Market stands as the largest and most influential pharmaceutical ecosystem in the world. According to Renub Research, the market is anticipated to expand from US$ 638.86 billion in 2024 to US$ 979.25 billion by 2033, registering a compound annual growth rate (CAGR) of 4.86% during 2025–2033. This sustained growth reflects the country’s unmatched strength in biomedical innovation, advanced healthcare infrastructure, and strong demand for cutting-edge therapies.

By Janine Root 20 days ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts4 days ago in Longevity

'20/20'

"Do It Again" the track that would ultimately open the Beach Boys final album on Capitol Records which was released on February 10th 1969 had originally been released as a single in August of 1968. The track was the first of many post-Pet Sounds era throwbacks to the early Beach Boys sound which would become continually more cliched and eventually lead the Beach Boys to the level of self-parody they would eventually succumb to in the 1980s while their closest contemporaries The Beatles nearing the end of their run in 1969 would go on to be viewed as the most influential band of all time. However, the song itself is not bad on its surface, and it opens with a futuristic sounding (for 1969) drumbeat captured by then-Beach Boys engineer Stephen Desper using tape delays on the drums performed by Dennis Wilson and John Guerin. The song has been re-recorded numerous times over the years on various Beach Boys-related projects most notably the 2011 re-recording at Capitol studios featuring the five surviving Beach Boys at the time backed instrumentally by various members of both the Brian Wilson Band and Mike Loves touring "Beach Boys" to promote the then upcoming Beach Boys 50th Anniversary reunion tour in 2012. The hammering and power drill sound at the end of the song was an excerpt from a track called "Workshop" that was to be a part of the uncompleted "SMiLE" album.

By Sean Callaghan6 days ago in Beat

Comments

There are no comments for this story

Be the first to respond and start the conversation.