How I tricked myself into paying off debt (and how you can, too)

I went from making late payments to paying extra.

The year is 2014, and I'm a recent college graduate.

I walked across the graduation stage on three hours of sleep, a Monster energy drink, and with a disdain for wearing a big black hat that messed up my perfect bangs.

I left the auditorium expecting to feel like I was on top of the world. I did it! I graduated after 3.5 years. Instead, I just wondered where we were going to dinner as a family, and why the outdoors were so bright and loud.

Then it hit me: I had no place to go. Where was I going to live? I was so obsessed with getting the best grades on these final exams that I completely forgot to consider my future.

What? Who does that?

Me.

I do.

I also get an internship in Los Angeles a few months later, even though I'm in Chicago, and I save $3,000, pack up my belongings, and take a credit card with me, "just in case."

Yeah. That turned in to maxing out $10,000 on a Chase Sapphire credit card pretty easily as I searched for a place to live in LA, hopping from hotel room to hotel room.

I'm not sure about you, but I think it's fine at this point to deduce that I was not the brightest crayon in the box.

Needless to say anything more about that story, I had a lot of debt:

- Student loan debt from a private, out-of-state art college.

- A 2011 Honda Civic car payment.

- Credit card debt from Victoria's Secret because I'm a sucker.

- Interest-free debt due to people I borrowed money from to stay afloat.

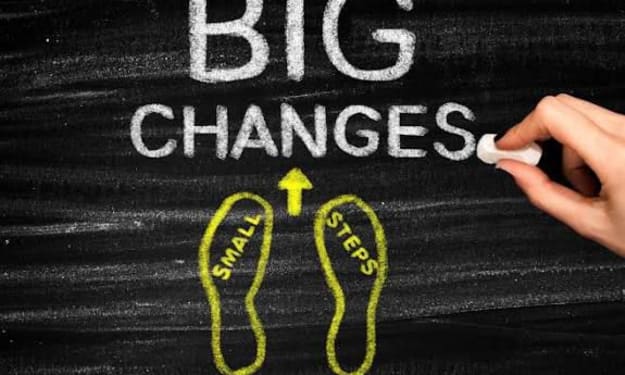

Hindsight is 20/20, my friends. However, there is a way that you can get out of debt, even if you don't have a job right now. Here is how I did it.

Make Yourself a Temperature Chart

We're going back to the basics. When's the last time you saw one of these? Elementary school? A fundraiser? The last time I saw it was at work. I figured that if professional adults were tracking progress using a temperature chart, they must be on to something.

And they were.

How to make your chart:

-Count how many lines there are. There's around 12 on my chart.

-Take your total debt. Divide that number by 12.

That's how many increments you're going to write on the chart and pay your debt in. You can make an incremental payment every month to get it paid off in a year, every week to make it faster, or throw money at it whenever.

The key is that there's a tangible number that you can visibly fill up with a bright, neon color of your choice. Keep the temperature chart hanging in a place where you pass it often (but not in front of company, so it doesn't make you feel guilty) and soon, you'll forget about what you had in your Amazon cart and instead, consider putting more money toward that bright streak of success.

I keep mine in my office. Nothing motivates me like reminding myself why I'm working in the first place. And once that debt is gone? We're FREE.

Organize Your Charts

Mark which charts have the highest APR, and write which number priority that chart is. The last thing you want to do is try to pay off each one all at once. I like to pay off the highest APR first, which is usually going to be a credit card, or a payday loan if you have one. Then, move on to the one with the second highest APR and so forth. You can also go in the order of which one will take the least amount of time, so you can get that feeling of success sooner than later.

It's All About the Mentality

I could sit and think about all of the things that I want to buy. I could plan for lavish vacations. I could go spend $50 on dinner every night this week. Or, I could fill up my temperature chart and get done with the damn thing. Once you're done paying off a debt, remove it from where it is hanging. It's gone! But keep it in a drawer to remind yourself of your progress on days when you feel like you're going nowhere.

It's very motivating to see your temperature chart fill up halfway. If you've made it that far, why can't you finish it? You totally can! It also helps to write where you're going to get the money from, and how often you're going to pay off each increment.

Can You Pay off Debt While You're Unemployed?

I'm going to be real with you here: that is real hard. You could freelance on Upwork, or take on a project for someone that you know in real life. But the reality is, you're going to need either two to three part-time jobs or one full-time job and a part-time job to really conquer debt. It all really depends on how much you make and how far you're in the hole. If you want to keep sane and pay debt off slower, just have one full-time job. If you want to take on a few fun projects, do that on the side and dedicate them directly to your debt.

I personally took a full-time remote writing job and a part-time remote data entry job so that way I could pay my bills and debt simultaneously. My money-maker is writing, but to avoid burnout, I took a mindless data entry job that was kind of like a "cool down" to my brain "workout" at the end of the day.

My advice is: Don't take on another job of the same thing you're already doing. If you're a cashier by day, take a dog sitting job by night. If you're a bank teller by day, be a cleaner by night. Don't work at McDonald's and then go work at Burger King, otherwise, you're going to hate yourself.

Plan Out Your Income vs. Out-Go

The momentum that I got from paying off my debt just from looking at and planning with my temperature chart was incredible! I wanted to make even larger payments on my car to finish off my temperature chart. I ended up paying off my car just a few months early, which was an amazing feeling.

Before I did that, I simply made sure I had enough money.

I planned what I was going to get for the month, and then I added up all of my bills. I planned $200 extra on top of my monthly food budget just in case, and I was realistic when I was planning out my "fun money." I then calculated how much I had left to give to my car loan that wouldn't make me feel broke. Maybe you know it by now, but writing out a budget or using an app like Every Dollar really helps.

There Really Is No Trick

There really isn't a "lifehack" to paying off your debt. It just requires you to plan and visualize your progress. You have to treat your debt like rent - it can't be late. You have to work around it so you can tackle it and move on to the next temperature chart. Gamification with these charts, which means to act as if it's a game, really helped me conquer my car payment and a credit card.

I never thought I would say this, but I can't wait to pay off the rest, including my student loan debt.

If you liked this article, please leave a heart or a tip if it works for you! Originally published on Medium.com.

About the Creator

Maddie M.

I'm a creative copywriter by day and a fiction/non-fiction writer by night.

You're alone, because you're lost

Being alone is a fear that one in three adults face WORLDWIDE. Why? Are we scared to be alone because we are faced with all of our thoughts we once tried to suppress? Or are we scared because we feel uncomfortable? Uncomfortable with the idea of being in a room with just you. You and your nasty thoughts. Thoughts like “Damn I should've apologized”, or “Why hasn't he texted me back?” or “I am a failure”. Yea. those thoughts. The forbidden thoughts that come sneak by the midnight hour, ...if you're lucky. You see loneliness doesn't have to be this way. It all starts with you.

By C⃣ h⃣ a⃣ n⃣ e⃣ l⃣6 days ago in Lifehack

Top tipple tricks

Been thinking a lot about drinking, lately. Not least because of a recent episode of over-indulgence and the inevitable after effects. Some readers may recall the earlier articles I wrote about beating the booze. Here I set out an experiment in techniques for cutting down on my alcohol intake. The experiment was successful, the techniques worked, and I have armed myself with an arsenal of weapons in the war against the demon drink. I have yet to fire the first round however. It's all a question of timing (perhaps procrastination).

By Raymond G. Taylor4 days ago in Psyche

Comments

There are no comments for this story

Be the first to respond and start the conversation.