Internet Banking in Uzbekistan: Comparative Analysis of Desktop Platforms – Kapitalbank, Octobank, Hamkorbank, and Others

The digitalization of Uzbekistan’s banking sector is gaining momentum. More and more clients are conducting transactions online, preferring internet banking as their primary channel of interaction with banks.

The digitalization of Uzbekistan’s banking sector is gaining momentum. More and more clients are conducting transactions online, preferring internet banking as their primary channel of interaction with banks. In this context, it is especially important to understand which banks offer truly convenient, functional, and secure remote banking solutions.

As part of an independent comparative study conducted by the international digital marketing agency The Digital Department, a comprehensive assessment was carried out of the internet banking services of leading financial institutions in Uzbekistan.

The purpose of the analysis was not to create a "top list" but to objectively compare the level of development of digital solutions in the banking sector.

The resulting ratings and profiles reflect the current state of internet banking and reveal the strengths and weaknesses of specific banks at the time of the study.

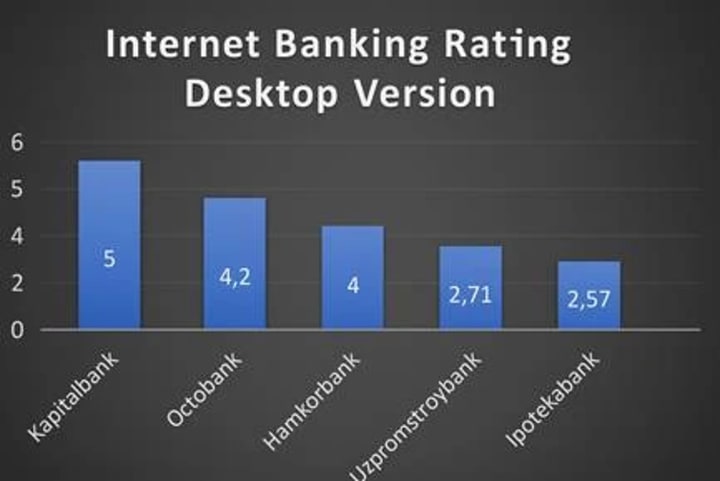

Results and Ratings

Based on the results of the analysis, all five banks demonstrated a comprehensive and balanced level of digital service development:

- Kapitalbank — 5.0

- Octobank — 4.2

- Hamkorbank — 4.0

- Uzpromstroybank — 2.71

- Ipotekabank — 2.57

General Conclusion

The results of the analysis show that the development level of desktop internet banking in Uzbekistan remains uneven. Some banks focus on broad digitalization, integration, and the evolution of user interfaces, while others provide only basic functionality with little emphasis on modern UX and technological advancement.

Kapitalbank confidently demonstrates leadership, offering a balanced combination of functionality, security, and digital maturity.

Octobank shows strong potential through its modern approach and focus on fintech solutions.

Hamkorbank also presents a stable and versatile product suitable for both individual and business clients.

Uzpromstroybank and Ipotekabank lag in technological advancement and user experience but remain viable tools for carrying out basic tasks. Their weaknesses primarily lie in interface design, system update frequency, and security standards.

Kapitalbank

Functionality

Kapitalbank offers one of the most comprehensive and well-balanced internet banking systems on the market in terms of functionality. Users can perform a wide range of operations: transfers between their own and external accounts, card top-ups and blocking, loan applications, and deposit openings.

The platform supports internal currency exchange, payment of all types of services (including government and utility bills), as well as taxes and fines. For business clients, extended features are available—automatic report generation, management of multiple accounts, mass payments, and integration with accounting systems.

Interface

The internet banking interface is designed in a modern, minimalist style. It is intuitive even for beginners. All key functions are accessible from the main dashboard, and the system easily adapts to the screen size and user preferences.

Security

Security is one of Kapitalbank’s strongest aspects. The system features multi-layered protection: HTTPS connection, two-factor authentication via apps (Google Authenticator, SMS, PUSH), and login monitoring by IP and device.

Biometric authentication is supported (including Face ID/Touch ID on paired devices), along with digital signatures. In case of suspicious activity, the system automatically initiates re-verification of the user.

Speed and Stability

The system performs with maximum stability. Regardless of the time of day, the platform maintains high transaction processing speeds. Even during mass transactions and peak load times (such as payroll days), performance remains unaffected.

Support

Kapitalbank’s support service demonstrates a high level of customer care. Multichannel communication is available: online chat on the website and within the platform, a 24/7 hotline, a Telegram bot, and a feedback service in the user account.

Operator response in chat typically arrives within 5–10 minutes. Most issues are resolved on the first contact. Users can track the status of their requests and receive guidance on specific transactions.

User Feedback

Kapitalbank’s internet banking receives high ratings from clients. Users highlight the platform’s stability, wide functionality, logical interface, and fast support.

Among the most praised features are the ability to open deposits or apply for loans online, and to save templates for recurring transactions. Criticism is minimal and usually related to personal technical limitations of individual users.

Technological Advancement

Kapitalbank actively invests in digital solutions. The internet banking platform receives regular updates: new features are introduced, processes are optimized, and innovative solutions are implemented—including API integrations with external services, subscriptions, cashback programs, and even AI-powered spending analytics.

The platform is synchronized with the mobile version, ensuring a unified user experience.

Average Score: 5.0

Kapitalbank offers one of the most complete internet banking systems in Uzbekistan. Users can make transfers, open deposits, apply for loans, manage subscriptions, currencies, and loyalty programs. The interface is intuitive and supports personalization. Security is high, with two-factor authentication, biometrics, and digital signatures. The system is stable, support is responsive, and technological development is actively ongoing.

Octobank

Functionality

Octobank offers a basic but stable set of functions in its desktop version. Users can view accounts and cards, make transfers between their own and external accounts, pay for services, and create payment orders.

Currency operations are supported, including access to current exchange rates and currency conversion. Templates for recurring payments are available. Business clients have access to bulk payment features, report exports, and both tax and contractual transactions.

For individual users, functionality is currently limited: there is no support for investment products, savings goals, or online purchases.

Interface

The interface is designed in a minimalist “fintech style,” free from excessive visual clutter. Main sections are laid out in a logical sequence, though new users may need time to adapt to the structure.

On certain small-screen devices, the interface may display incorrectly—buttons may shift off-screen, and dropdown menus may not expand properly. Despite this, the overall visual concept is modern and appealing.

Security

The system is protected by standard measures: HTTPS connection, data encryption, and transaction confirmation via SMS or email codes.

However, there is no two-factor authentication via applications (e.g., Google Authenticator). There is also no biometric login or digital signature support for individual users. A stricter access policy is implemented for business users.

Speed and Stability

During normal hours, the system runs stably. The interface responds quickly to user actions, and pages load without noticeable delays.

During peak periods (e.g., morning hours or end of month), occasional issues may occur: loading of transaction history may slow down, and server-side errors may appear. These problems are intermittent but affect the overall perception of quality.

Support

Octobank provides support via online chat, initially handled by a bot. A human operator is connected if needed. There is also a “Submit a request” form and a support hotline.

The average response time ranges from 15 to 60 minutes. On weekends and outside business hours, operator availability may decrease. Support functions properly but is not always prompt.

User Feedback

Clients positively note the modern interface and Octobank’s overall commitment to digitalization. The business-oriented functionality and convenience of templates are particularly appreciated.

Technological Advancement

Octobank positions itself as a digital-first bank. API integrations are supported, there is potential for scaling, and the technical foundation for connecting external solutions is already in place.

Average Score: 4,2

Octobank is focused on a digital approach and fintech-style interface. Transfers, bill payments, templates, and business functions are supported. The interface is minimalist but needs improved navigation. Security is basic—2FA via apps is not implemented. Occasional slowdowns occur during peak times. It is well-suited for businesses but requires further development for individual clients.

Hamkorbank

Functionality

Hamkorbank offers a wide range of services for both individual and corporate clients. In the desktop version, users can transfer funds between their own and external accounts, pay utility and government bills, perform currency operations, open deposits, and apply for loans. Business clients have access to account management, report generation, and both tax and bulk payments.

Interface

The internet banking interface is structured in a concise and logical manner. Main functions are placed on the main dashboard, and navigation is straightforward. The visual style meets modern standards, and the interface adapts to various screen sizes.

Security

Hamkorbank implements comprehensive security measures: secure HTTPS connection, two-factor authentication (via SMS codes and PUSH notifications), and monitoring of suspicious activity.

Digital signature support is available for business clients. All actions within the system are logged, and transaction confirmation is mandatory. The security level of the internet bank complies with modern standards.

Speed and Stability

The system operates stably. Even during peak hours, the platform maintains its performance and the interface runs smoothly. The speed of loading transaction history, processing payments, and navigating between sections is high.

Scheduled updates are conducted during nighttime hours and do not disrupt user activity.

Support

Customer support is available through online chat, a feedback form on the website, and via phone. The average response time is within 10–20 minutes. Operators are competent, and for more complex queries, specialized experts are involved.

Support operates in a mode close to 24/7, which is especially important for business clients.

User Feedback

Users positively evaluate the system’s stability, reliability, convenient interface, and broad functionality. Some suggestions include speeding up chat support and adding more analytical tools.

Overall, Hamkorbank is perceived as a modern and user-friendly bank with a focus on versatility.

Technological Advancement

The bank is actively developing its digital platform. Updates are released regularly, and new features are added. API integrations have been implemented, and data exchange with accounting systems has been improved.

Hamkorbank is committed to digital transformation, including through partnerships with fintech platforms.

Average Score: 4.0

Hamkorbank offers a balanced internet banking experience for both private and business clients. Transfers, bill payments, deposits, currency management, and account operations are supported. The interface is user-friendly, transaction security is ensured, platform performance is stable, and support is available through multiple channels. Updates are released regularly.

Uzpromstroybank

Functionality

Uzpromstroybank's internet banking offers a basic set of functions: transfers between accounts, payment of utility and government services, viewing statements, and generating payment orders. Corporate clients have access to settlement operations, report exports, and tax payments.

However, extended capabilities are lacking—there is no online deposit opening, loan applications, investment products, or automatic payment settings. The functionality covers essential needs but does not go beyond standard banking operations.

Interface

The interface of the system is visually outdated. The design is not adapted to modern UX/UI standards. Sections are overloaded with information, and the navigation structure requires getting used to.

Security

The system uses basic protection tools: login and password authorization, and operation confirmation via SMS. Work with digital signatures is available only for corporate clients.

Additional protection mechanisms—such as 2FA via apps, biometrics, device management, or geolocation restrictions—are absent. This reduces the level of trust in the system among more demanding users.

Speed and Stability

The internet bank generally functions stably, but the system is prone to slowdowns during peak loads. This is particularly evident when working with statements, generating reports, and sending payment orders.

Support

The support service operates during standard business hours. Feedback is provided via phone and an online form. The average response time ranges from 30 minutes to several hours.

Support rarely goes beyond standard templates. In more complex technical cases, a visit to a branch may be required.

User Feedback

Client reviews are mostly neutral. Reliability and logical transaction flow are noted by long-time users. However, many complain about the outdated interface, limited functionality, and lack of a convenient mobile counterpart.

User satisfaction is lower than that of more innovative competitors, though basic loyalty remains.

Technological Advancement

The pace of technological development of the internet bank is slow. The interface is rarely updated, and the implementation of new features is infrequent. Integration with external services and process automation are at an early stage.

There is potential for development: a basic digital infrastructure is in place, but its realization requires prioritized attention.

Average Score: 2.71

Uzpromstroybank offers basic functionality: transfers, statements, and payment orders. The interface is outdated and requires time to master. Security is standard, lacking modern two-factor authentication. The system works stably but not always quickly. Support is not always responsive. Updates are irregular.

Ipotekabank

Functionality

Ipotekabank’s internet banking offers a limited set of features. The system allows for transfers between accounts, payment of utility and standard services, viewing balance and transaction history.

The platform does not support online deposit openings, loan applications, investment products, or subscriptions. There is no flexibility for setting up recurring payments. The functionality is more suited to occasional basic operations than to systematic digital financial management.

Interface

The interface requires modernization. It is overloaded with outdated elements, not adapted to various devices, and does not follow modern UX/UI principles.

Navigation between sections is not intuitive, and visual highlights are poorly implemented. Users experience difficulty in locating necessary functions. Working with the system may cause frustration among new clients.

Security

The security level of Ipotekabank’s internet banking meets only minimal standards. Login and password are used, along with SMS-based operation confirmation.

Two-factor authentication via apps, biometric authentication, or digital signatures are not supported. Users do not receive alerts about suspicious activity. This makes the platform vulnerable to potential threats.

Speed and Stability

System performance is unstable. There may be long delays when loading transaction history or switching between sections. Interface freezes are frequent.

The platform is prone to outages during peak hours. System updates occur without prior notification, causing temporary unavailability of functions.

Support

Customer support is limited. Average response time ranges from 30 minutes to several hours. Communication channels include a feedback form and a hotline, but it is often difficult to get through by phone.

Many issues can only be resolved by visiting a branch, which reduces the convenience of service.

User Feedback

Reviews from open sources are mostly restrained and critical. Users acknowledge the presence of basic features but point to the outdated interface, frequent technical issues, and lack of digital flexibility.

Some note that they switch to the mobile app, as the desktop version is less convenient.

Technological Advancement

The platform’s technological development is slow. Updates are irregular, and major interface improvements have not been implemented. The desktop version lags even behind the bank’s mobile app.

There are no API integrations, and automation is minimal. The platform requires a full-scale digital transformation.

Ipotekabank — Average Score: 2.57

Ipotekabank offers a basic set of functions: transfers, service payments, and balance viewing. The interface is inconvenient and visually outdated. Security is minimal — only SMS confirmation. The platform is unstable, with potential crashes and delays. Support is slow, and users report a lack of modern solutions.

Overall, the internet banking market in Uzbekistan is undergoing active transformation. The demand for more flexible, secure, and visually comfortable digital solutions is growing, and this will define the competitive edge of banks in the coming years.

About the Creator

Keep reading

More stories from Susan Scava and writers in Journal and other communities.

The goals I did not achieve

Every writing goal I made for the year is a wash. It has been this way for a while, but I think it's important to be open about my failures and the reality of how life can get in the way. This is especially true considering the several times I have posted on Vocal about my writing goals, how I was changing my approach, and where I was hoping to be for the upcoming year. I will probably do that again in a couple months, but for now, it is time to acknowledge where I am today.

By Kay Husnick24 days ago in Journal

AcehGround: A Leading Voice for News in Aceh and Beyond

In Indonesia's northernmost province of Aceh, staying connected to local events, governance developments, cultural stories, and national issues remains essential for residents, businesses, and visitors. AcehGround has established itself as a prominent online news portal dedicated to providing up-to-date coverage across these areas. Operating primarily through its website, acehground.com, the platform focuses on delivering Berita Aceh—news from the region—while also incorporating national and international stories relevant to local audiences.

By Eliana Daisy4 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.