Australia’s E-Wallet Market: From Convenience to Everyday Essential

With rising digital payments, security demands, and seamless integration into services, e-wallets are transforming how Australians pay, save, and live.

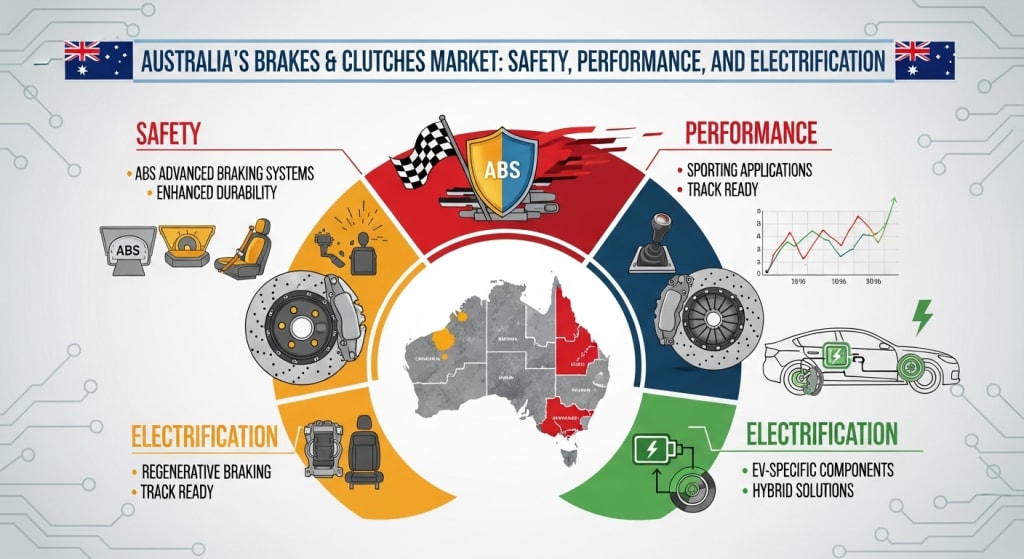

The Australia brakes and clutches market was valued at approximately USD 24.5 million in 2024. By 2033, it is projected to grow to around USD 40.0 million, reflecting a compound annual growth rate (CAGR) of about 5.6% over 2025–2033.

Market Growth Drivers:

Stricter Safety Regulations

Vehicle safety is increasingly regulated in Australia. Mandates and standards requiring features such as Anti-lock Braking Systems (ABS), Electronic Stability Control (ESC), and Electronic Brake-force Distribution (EBD) are pushing manufacturers to upgrade braking systems. These technologies are becoming standard even on mid-range models. The need for reliable braking under various driving conditions (wet roads, emergency braking, downhill driving) further lifts demand.

Surge in Electric and Hybrid Vehicles

Electric (EV) and hybrid vehicles are changing the role of brakes. Regenerative braking reduces wear on friction brakes but demands compatible components and materials. Braking systems must adapt to offer both performance and durability, especially where friction braking is used. Hybrid vehicles also often include systems that blend traditional and regenerative braking, which adds complexity and places higher demands on component design.

Advances in Clutch Technology

On the clutch side, demand for smoother, more efficient transmission systems is rising. Dual-clutch transmissions (DCTs) and automated manual transmissions (AMTs) are gaining market share. These systems provide improved driver comfort, better fuel efficiency, and quicker gear shifts. As consumers increasingly prefer performance and convenience, these clutch types are becoming more common, especially in premium vehicles.

Aftermarket & Fleet Replacement Needs

Australia has an aging vehicle fleet, especially in commercial, agricultural, and industrial sectors. Many vehicles operate for years, creating ongoing demand for replacement brake pads, discs, clutch plates, and full systems. As OEM warranties expire, maintenance and repair (MRO) services become more important. The aftermarket sector is thus a backbone of continuous demand.

Industrial and Off-Highway Applications

Heavy-duty vehicles (mining, construction, agriculture) demand robust braking and clutch systems that can resist wear, heat, and harsh conditions. These segments require higher-capacity clutches and brakes, often with safety and durability priorities. Infrastructure and industrial development support the growth of these segments.

Get a PDF Report Sample: https://www.imarcgroup.com/australia-brakes-clutches-market/requestsample

Real-World Trends & Examples

- More manufacturers are integrating advanced braking systems as standard equipment rather than optional extras. Vehicles for public transport or fleet operators often lead this trend.

- Brake pad and rotor producers are working on materials that resist heat, offer better stopping distances, and generate less noise and dust.

- Clutch manufacturers are investing in lighter, more durable materials and technologies that reduce inertia and improve fuel efficiency.

- Repair shops and service centers are adapting to increased complexity—technicians need training to maintain, diagnose, and replace components in hybrid/Electric/AMT/DCT systems.

Key Challenges and Headwinds

High Development Costs & Material Expenses

Advanced braking and clutch components—especially those compatible with EVs or high-performance vehicles—require more expensive materials (ceramics, composites, high-grade metals). R&D costs for integrating systems such as regenerative braking or dual-clutch setups are high, and smaller manufacturers may find cost and scale a barrier.

Regulatory and Certification Complexity

Meeting safety standards requires testing, quality assurance, and certification. As systems become more complex (e.g. incorporating electronics, sensors), the regulatory burden increases. Differences across state or territory regulations may add complexity for companies that operate nationally.

Changing Wear Patterns & Maintenance Cycles

Because regenerative braking reduces usage of conventional friction brakes, components may last longer but could also suffer from different wear and usage patterns. This requires different maintenance schedules, aftermarket strategies, and possibly changes in how service providers operate.

Competition and Price Sensitivity

Aftermarket segments are competitive, and customers often compare cost vs performance vs durability. Premium materials or advanced designs may be preferred, but only if prices and service availability are acceptable. Also, import competition and spare-parts availability affect margins and consumer choices.

Emerging Opportunities

OEM Supplier Partnerships

Component suppliers that partner directly with automakers to co-develop braking and clutch systems, especially for EVs and hybrids, can better specify performance, safety, materials, and durability. Early collaboration offers advantages in specification compliance and scale.

Material Innovation & Eco-Friendly Design

Demand for lighter, more sustainable materials offers room for innovation—low dust brake materials, recyclable components, and manufacturing processes with lower environmental footprints will appeal to both regulators and consumers.

Fleet Electrification & Regenerative Braking Systems

As commercial fleets, public transport, and delivery vehicles move toward electrification, the opportunities for regenerative braking systems, and thus for specialized brake materials and designs, increase. Maintenance providers and parts makers that adapt to this shift will have an edge.

Service & Diagnostic Expertise

With more complex systems in modern vehicles, workshops with advanced diagnostics for ESC, ABS, dual-clutch/AMT systems, and regenerative braking will be in demand. Training, tooling, and specialization are key.

Premium / Niche Performance & Specialty Vehicles

Performance cars, off-roaders, motorsports, luxury segments want higher quality, responsive benchmarks. Custom brakes/clutches, carbon-ceramic materials, noise/vibration suppression, lightweight alloys—all are opportunities in premium niches.

Ask An Analyst: https://www.imarcgroup.com/request?type=report&id=35300&flag=C

Brake and clutch systems are central to safety, efficiency, and driver experience. As Australia shifts toward stricter safety norms, more EV/hybrid sales, and higher consumer expectations, the brakes & clutches market is not just about stopping the vehicle—it’s about how vehicles integrate safety, performance, sustainability, and value.

With a projected size of USD 40 million by 2033, the market is modest but growing steadily. The growth may be faster in specific segments (EV compatible systems, aftermarket, industrial applications) than in others. For manufacturers, component makers, and service providers, staying ahead means embracing innovation, quality, regulatory compliance, and strategic partnerships.

About IMARC Group

IMARC Group delivers detailed market analysis and strategic guidance. Their report on the Australia Brakes & Clutches Market includes segmentation by technology (electric, mechanical, pneumatic/hydraulic, electromagnetic), product type (dry vs oil-immersed), sales channel (OEM vs aftermarket), end-use industry, and regional analysis—helping stakeholders map where to invest, manufacture, or specialize.

About the Creator

Kevin Cooper

Hi, I'm Kavin Cooper — a tech enthusiast who loves exploring the latest innovations, gadgets, and trends. Passionate about technology and always curious to learn and share insights with the world!

Keep reading

More stories from Kevin Cooper and writers in Journal and other communities.

Australia’s Firearms Market: Between Regulation and Demand

Australia’s firearms market was valued at approximately USD 1.16 billion in 2024. The market is projected to grow to about USD 2.40 billion by 2033, at a compound annual growth rate (CAGR) of 7.50% over 2025–2033.

By Kevin Cooper6 months ago in Journal

Author’s Advice

If you would’ve asked me 20 years ago did I know I’d become a writer and an author, I would’ve said “nope, ain’t happening”. As fate would have it I did become an author and I can honestly say I’m loving it so far. It really does feel good to be a writer. I’ve learned a lot on this journey and I feel like with even me being as new to this world as I am, there’s some wisdom I need to share with every other aspiring author.

By Joe Patterson4 days ago in Journal

Strategic Buyers In Behavioral Healthcare

Introduction The behavioral healthcare sector has experienced significant growth over the past decade, attracting strong interest from strategic buyers. Strategic buyers are organizations already operating within healthcare or related industries that acquire behavioral health companies to expand services, strengthen market presence, or improve care integration. These buyers usually focus on long-term operational benefits rather than short-term financial gains. As demand for mental health and addiction treatment services continues to rise, strategic buyers are increasingly involved in acquisitions and partnerships across the behavioral healthcare market.

By Abdul Mueed6 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.