US Remote Patient Monitoring Market Surges to $29.13 Billion by 2030

Digital Transformation and Value-Based Care Models Drive 12.6% CAGR Growth as C-Suite Executives Prioritize Connected Patient Monitoring Technologies

The Remote Patient Monitoring (RPM) market in the United States is evolving rapidly, becoming a fundamental element of contemporary healthcare systems and a key focus for healthcare leaders across the country. The market was worth $14.15 billion in 2024 and is expected to grow to $16.09 billion in 2025. Forecasts indicate a strong compound annual growth rate (CAGR) of 12.6% until 2030, with a total market value of $29.13 billion anticipated by the close of the decade.

Download PDF Brochure of US Remote Patient Monitoring (RPM) Market

What's fueling this remarkable expansion? The intersection of FDA-cleared wearable tech, mobile health apps, and cloud-based monitoring systems is fundamentally altering how patient care is delivered. Healthcare leaders are starting to see remote patient monitoring as a strategic necessity, not just a short-term fix. It's a solution that directly tackles rising healthcare expenses, the difficulties of managing chronic diseases, and the operational limits that health systems nationwide are grappling with.

Why does this matter to healthcare leaders right now?

As value-based care moves from being a goal to a practical approach, remote patient monitoring (RPM) technologies are allowing healthcare providers to keep tabs on patients around the clock, outside of the usual office visits. This is a big deal for CFOs who want to cut costs, CMOs aiming to stand out from the competition, and CEOs trying to deal with the tricky world of getting paid while still delivering good care. The rise of hospital-at-home programs, along with the use of artificial intelligence and cloud analytics in RPM systems, is turning these tools from nice-to-haves into vital parts of the healthcare system of the future.

Strategic Market Segmentation Reveals Investment Priorities

When examining component-level performance, the software segment emerges as the fastest-growing category, projected to register the highest CAGR of 14.6% during the forecast period. This growth trajectory signals a fundamental market shift where data integration, analytics capabilities, and interoperability increasingly determine competitive advantage. The devices segment, however, continues to represent the largest market share as of 2024, driven by continuous technological advancements in wearable sensors, blood pressure monitors, glucose meters, pulse oximeters, and cardiac monitoring equipment.

Where is clinical adoption most concentrated? Cardiology applications commanded 29.0% of the US RPM market in 2024, reflecting the critical intersection of high disease prevalence, favorable reimbursement structures, and proven clinical efficacy. RPM technologies in this segment enable early detection of cardiac complications, medication adherence monitoring, and hospitalization prevention—delivering measurable ROI that resonates with both clinical and financial stakeholders.

Who are the end users driving demand? While healthcare providers currently dominate market utilization, the patients segment is expected to register the highest CAGR of 13.1% during the forecast period. This shift underscores the democratization of healthcare technology and the growing consumer expectation for home-based, digitally enabled care experiences. For pharmaceutical, biotechnology, and MedTech companies, this trend presents partnership opportunities and new distribution channels as patient-directed care becomes mainstream.

Competitive Landscape: Established Leaders and Emerging Disruptors

How is the competitive landscape evolving? Koninklijke Philips N.V., OMRON Healthcare Inc., and Medtronic maintain star positioning in the US RPM market, leveraging strong market share and comprehensive product portfolios. Their leadership reflects sustained investment in clinical validation, regulatory compliance, and enterprise-grade integration capabilities—factors that resonate with risk-averse health system CIOs and procurement executives.

However, emerging players including CareSimple Inc., TimeDoc, Inc., and MD Revolution Inc. are distinguishing themselves within specialized niches, demonstrating that market entry barriers are lowering for innovative, focused solutions. These companies represent potential acquisition targets or partnership opportunities for established enterprises seeking to accelerate innovation timelines and access specialized capabilities.

Market Forces Shaping Executive Strategy

What trends are influencing customer operations? End users—including hospitals, ambulatory centers, home health organizations, and insurance companies—are navigating complex operational pressures including changing patient expectations, value-based care mandates, and shifting service delivery models. The acceleration of home health services, chronic patient management requirements, and digitally oriented care delivery, combined with reimbursement complexities and data protection imperatives, are driving demand for scalable, interoperable, AI-powered RPM platforms.

Key Drivers Fueling Market Expansion

The digital transformation of patient care across the US healthcare system represents the primary growth catalyst. Healthcare organizations are integrating RPM with electronic health records, telehealth platforms, and virtual care solutions to enable proactive chronic disease management, post-discharge monitoring, and hospital-at-home models. This patient-centric approach improves clinical access while reducing in-person encounters—a dual benefit that addresses both quality and cost objectives for healthcare executives.

The growing adoption of hospital-at-home and advanced care-at-home models presents a significant market opportunity. Healthcare organizations are deploying RPM technology platforms to deliver acute and post-acute care in patients' homes, providing constant observation and real-time clinical notifications. This capability relieves inpatient capacity constraints while curbing healthcare expenditure—strategic imperatives for health system CEOs and COOs managing post-pandemic operational challenges.

Critical Challenges Requiring Executive Attention

What obstacles must leaders navigate? Interoperability limitations and EHR integration challenges within US healthcare systems remain principal restraints. Many RPM solutions cannot seamlessly integrate with dominant EHR platforms, creating health information silos that undermine clinical workflow efficiency. Fragmented reimbursement policies and complex billing requirements add administrative burden and financial uncertainty.

Data privacy, cybersecurity, and HIPAA compliance concerns present ongoing governance challenges for CISOs and risk management executives. Additionally, the limited integration of social determinants of health into RPM programs represents a strategic gap, particularly for vulnerable populations where housing, nutrition, connectivity, and support significantly impact clinical outcomes.

Real-World Applications Delivering Measurable ROI

Leading healthcare organizations are deploying RPM solutions to achieve tangible business results. Abbott's continuous glucose monitoring systems and cardiac monitors demonstrate widespread clinical acceptance and improved patient outcomes. Medtronic's MyCareLink Smart and Vital Sync platforms enable early complication detection and reduced hospital stays. Boston Scientific's CardioMEMS HF System has proven effectiveness in cutting heart failure hospitalizations and mortality rates. GE Healthcare's integration of acute monitoring with home-based virtual care extends hospital-grade capabilities beyond facility walls, improving capacity utilization and reducing readmissions.

Market Ecosystem and Strategic Partnerships

The US RPM market encompasses equipment manufacturers, wearable device developers, software solution providers, connectivity and cloud services platforms, and diverse end-user stakeholders. Real-time health information captured through these solutions transmits via cloud infrastructure and integrates with clinical systems, enabling remote health service delivery. The demand originates from stakeholders seeking improved healthcare outcomes and cost-effective, home-based care alternatives—strategic objectives that align with executive priorities across payer and provider organizations.

Recent Strategic Developments

February 2025: Teladoc Health acquired Catapult Health to strengthen chronic illness management capabilities by combining at-home testing, telehealth solutions, and monitoring-enabled preventive healthcare services.

October 2025: Koninklijke Philips N.V. established a strategic collaboration with Hoag Health System to standardize and optimize patient monitoring across two acute care hospitals, implementing Philips' Equipment Management as a Service (EMaaS) Solution and PIC iX Central Monitoring System.

December 2025: Artella Solutions and VivaLNK formed a partnership delivering end-to-end ambulatory cardiac monitoring solutions, integrating VivaLNK's wearable ECG technologies with Artella's real-time cardiac monitoring Software-as-a-Service platform.

Strategic Implications for C-Suite Executives

For healthcare CEOs, CFOs, and CMOs, the US RPM market represents both opportunity and necessity. Organizations that strategically deploy interoperable, AI-enabled RPM platforms position themselves to capture value-based care incentives, optimize operational efficiency, and differentiate their service offerings in increasingly competitive markets. The convergence of regulatory support, technological maturity, and demonstrated clinical efficacy has created an inflection point where RPM transitions from emerging technology to essential infrastructure.

Investment decisions should prioritize solutions offering robust EHR integration, comprehensive data security, flexible reimbursement alignment, and proven clinical validation. Strategic partnerships with established platform providers or targeted acquisitions of specialized innovators represent viable pathways for accelerating capability development and market positioning.

Market Intelligence and Strategic Planning

The comprehensive market analysis encompasses revenue forecasts, competitive rankings, ecosystem mapping, regulatory assessments, and reimbursement pathway evaluations across device, software, and services segments. Coverage includes cardiology, diabetes, oncology, neurology, sleep disorders, wellness improvement, respiratory disorders, mental health, and additional clinical indications, serving healthcare providers, payers, patients, pharmaceutical companies, biotechnology firms, and MedTech organizations.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

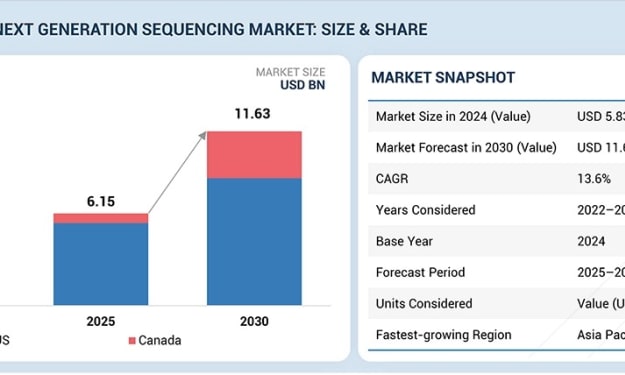

North America Next-Generation Sequencing Market Poised to Double to $11.63 Billion by 2030

The North American next-generation sequencing (NGS) market is entering a transformative growth phase, advancing from $6.15 billion in 2025 to a projected $11.63 billion by 2030, representing a compound annual growth rate (CAGR) of 13.6%. This acceleration signals a fundamental shift in how healthcare systems, biopharmaceutical enterprises, and research institutions approach disease diagnosis, drug development, and patient stratification.

By Juan Martinezabout 6 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight27 days ago in Futurism

Energy Bar Market: Plant-Based Nutrition, Healthy Snacking & Global Growth Trends

People are eating more energy bars because they want to stay healthy, are busy, and need quick nutrition. More people are doing fitness, sports, and outdoor activities, which increases demand. New bars with natural ingredients, high protein, and extra health benefits are becoming popular with health-conscious consumers. According to IMARC Group's latest research publication, The global energy bar market size reached USD 3.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 6.5 Billion by 2033, exhibiting a growth rate (CAGR) of 5.68% during 2025-2033.

By James Whitmanabout 8 hours ago in Futurism

The Duelist

The rays of a dying red sun flashed against the onrushing blade. The grey beards say the key to dueling lies in size, speed, reach, righteous fury, whatever the person in front of them pays them to say. Matteo knew better than any it was none of these and had an undefeated record on these sands to prove it.

By Matthew J. Fromm3 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.