Hydrogen Generation Market: Blue, Green & Gray Hydrogen Pathways & Global Supply Dynamics

Hydrogen generation gains traction in power, transport, and industrial applications.

According to IMARC Group's latest research publication, global hydrogen generation market size reached USD 181.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 279.8 Billion by 2034, exhibiting a growth rate (CAGR) of 4.93% during 2026-2034.

How AI is Reshaping the Future of Hydrogen Generation Market

- Predictive Production Optimization: AI algorithms analyze real-time sensor data from electrolyzers and reforming units to optimize hydrogen production parameters. Machine learning models predict equipment failures before breakdowns, reducing downtime by up to 30% while maximizing operational efficiency across production facilities.

- Energy Management and Grid Integration: AI-powered systems balance renewable energy inputs with hydrogen production schedules, automatically adjusting electrolyzer operations based on electricity prices and solar/wind availability. Smart algorithms optimize energy consumption patterns, cutting production costs while supporting grid stability.

- Quality Control and Safety Monitoring: Computer vision and machine learning detect anomalies in hydrogen purity, pressure fluctuations, and storage conditions in real-time. AI systems monitor safety parameters across production and distribution networks, identifying potential hazards and preventing incidents through predictive analytics.

- Supply Chain and Distribution Intelligence: AI analyzes demand patterns across industrial, transportation, and power sectors to forecast hydrogen requirements with remarkable accuracy. Smart logistics platforms optimize delivery routes, storage allocation, and refueling station inventory, ensuring efficient distribution while minimizing waste.

- Process Innovation and Carbon Tracking: AI accelerates research into cost-effective production methods by simulating thousands of catalyst configurations and electrolyzer designs. Advanced analytics track carbon footprints throughout the hydrogen value chain, enabling producers to certify green hydrogen credentials and meet sustainability standards.

Access the Sample Report for Current Insights and Forecasts

Hydrogen Generation Industry Overview:

Government initiatives worldwide are fundamentally reshaping the hydrogen landscape through massive investments and supportive policies. India's National Green Hydrogen Mission secured Rs 600 crore funding in Budget 2024-25, doubling from Rs 300 crore the previous year, as part of a larger Rs 19,744 crore outlay through FY 2029-30. The United States finalized Section 45V clean hydrogen production tax credits in January 2025, while the European Union allocated €1.2 billion through its Hydrogen Bank initiative in December 2024, targeting renewable hydrogen across the European Economic Area. China aims to achieve 100,000-200,000 tonnes green hydrogen production capacity by 2025, with its first underground hydrogen storage facility operational in Hubei province. These coordinated policy frameworks are creating a robust foundation for hydrogen infrastructure development, electrolyzer manufacturing capacity expansion, and large-scale adoption across transportation, industrial, and power generation sectors globally.

Hydrogen Generation Market Trends & Drivers:

- Industrial decarbonization mandates are driving unprecedented hydrogen adoption across heavy manufacturing sectors. Global hydrogen demand reached 97 million tonnes in 2023 and continues climbing as refineries, steel plants, and chemical manufacturers transition from fossil fuels. India inaugurated its first green hydrogen plant at GAIL's Vijaipur facility in July 2024, producing 4.3 tonnes daily using 10 MW electrolyzers, while Adani Group began blending 2.2-2.3% green hydrogen into natural gas pipelines serving households in Shantigram, Ahmedabad. Japan and South Korea are advancing hydrogen-based electricity generation through major demonstration projects and government-established auctions. The transportation sector generated 15,000 tonnes of CO2 removal annually through hydrogen fuel cell applications, with particular momentum in heavy-duty vehicles, maritime shipping, and aviation where battery alternatives face limitations. These industrial commitments create consistent baseload demand that supports long-term infrastructure investments.

- Technological breakthroughs are rapidly improving hydrogen production economics and accessibility. Electrolyzer costs have declined substantially as manufacturers achieve economies of scale, with India's Production-Linked Incentive schemes attracting 1,500 MW electrolyzer manufacturing capacity commitments from eight companies by May 2024. Advanced alkaline and PEM electrolyzer systems now offer improved efficiency and faster response times, enabling better integration with variable renewable energy sources. China unveiled a trading platform for net-zero hydrogen and derivatives in July 2024, establishing market mechanisms that enhance price transparency and liquidity. Hybitat launched residential-scale green hydrogen generation and storage systems in November 2024, with the first 200 kWh unit converting excess solar power into storable hydrogen for later electricity generation or gaseous use. Blue hydrogen projects incorporating carbon capture technologies are expanding across gas-rich regions, with Air Liquide receiving €114 million from the European Innovation Fund for its ENHANCE project in Belgium, demonstrating pathways to low-carbon production from existing natural gas infrastructure.

- Infrastructure development and international collaboration are accelerating market growth and establishing hydrogen trade corridors. Germany is constructing a €24 billion backbone pipeline network enabling large-scale hydrogen distribution, while major ports in India including Deendayal, Paradip, and V.O. Chidambaranar are being developed as Green Hydrogen Hubs through phased implementation. NTPC's €19.7 billion green hydrogen hub in Andhra Pradesh, scheduled for 2027 completion, will integrate 20 GW renewable capacity producing 1,500 tonnes daily. Cross-border partnerships are emerging as countries leverage complementary strengths—Australia and Middle Eastern nations with abundant solar resources are positioning as hydrogen exporters to Asian and European markets with strong industrial demand. Malaysia and Indonesia are developing ammonia export corridors targeting Japanese and Korean buyers, while China's dedicated hydrogen pipeline connecting Inner Mongolia to coastal zones represents the world's largest such infrastructure. These strategic partnerships and export frameworks are establishing hydrogen as a globally traded energy commodity, similar to LNG markets, creating standardized quality specifications and enabling economies of scale that drive costs toward fossil fuel parity.

Leading Companies Operating in the Global Hydrogen Generation Industry:

- Air Liquide International S.A.

- Air Products Inc.

- CLAIND srl

- INOX Air Products Ltd.

- Linde Plc

- Mahler AGS GmbH

- McPhy Energy S.A.

- Messer Group GmbH

- NEL Hydrogen

- Taiyo Nippon Sanso Corporation

- Weldstar Inc.

- Xebec Adsorption Inc.

Hydrogen Generation Market Report Segmentation:

By Technology:

- Coal Gasification

- Steam Methane Reforming

- Others

Steam methane reforming represents the largest segment, as it offers economical and efficient large-scale hydrogen production using established infrastructure.

By Application:

- Methanol Production

- Ammonia Production

- Petroleum Refinery

- Transportation

- Power Generation

- Others

Ammonia production dominates the market owing to extensive fertilizer manufacturing demand and emerging role as a hydrogen carrier for energy storage.

By Systems Type:

- Merchant

- Captive

Merchant reforming holds the largest market share due to scalability and ability to serve diverse industries without requiring on-site production infrastructure.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific dominates the hydrogen generation market due to robust industrial base, aggressive decarbonization targets, and government-backed green hydrogen initiatives.

Recent News and Developments in Hydrogen Generation Market

- November 2024: Hybitat Srl, a unit of SIT Group, launched a green hydrogen generation and storage system for residential, commercial, and public use. The first 200 kWh system will be installed in an 18th-century residence in 2025, using excess solar power to produce hydrogen for later conversion into electricity or gaseous applications.

- October 2024: Adani Group began blending 2.2-2.3% green hydrogen into natural gas supplied to households in Shantigram, Ahmedabad, as part of efforts to reduce emissions and achieve net-zero targets. The initiative, led by Adani Total Gas Ltd in partnership with TotalEnergies, injects hydrogen produced through clean methods into existing natural gas pipelines.

- July 2024: Tecnimont Private Limited and NEXTCHEM inaugurated India's first green hydrogen production plant for GAIL (India) Limited at Vijaipur, Madhya Pradesh. The facility produces 4.3 tonnes of green hydrogen daily using 10 MW electrolyzers, marking GAIL as the first company in India to begin megawatt-scale green hydrogen production.

- April 2024: Panasonic's Electric Works Company launched the PH3 pure hydrogen fuel cell generator for Europe, Australia, and China. The generator uses high-purity hydrogen and oxygen chemical reactions to generate power, expanding Panasonic's hydrogen business beyond Japan following the 2021 launch of the 5 kW PH1 model.

- February 2024: India's Ministry of New & Renewable Energy released scheme guidelines facilitating pilot projects for green hydrogen use in buses, trucks, and four-wheelers under the National Green Hydrogen Mission. The program received Rs 496 crore budgetary allocation through financial year 2025-26 to advance hydrogen mobility solutions.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

sujeet. imarcgroup

With 2 years of hands-on experience at IMARC Group, I have conducted in-depth market research and analysis across diverse industries including technology, healthcare, agriculture, and consumer goods.

Keep reading

More stories from sujeet. imarcgroup and writers in Futurism and other communities.

Aircraft Cabin Interior Market: Premium Cabin Demand, Luxury Interiors & Global Aviation Trends

According to IMARC Group's latest research publication, the global aircraft cabin interior market size reached USD 31.1 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 56.2 Billion by 2033, exhibiting a growth rate (CAGR) of 6.47% during 2025-2033.

By sujeet. imarcgroup3 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight18 days ago in Futurism

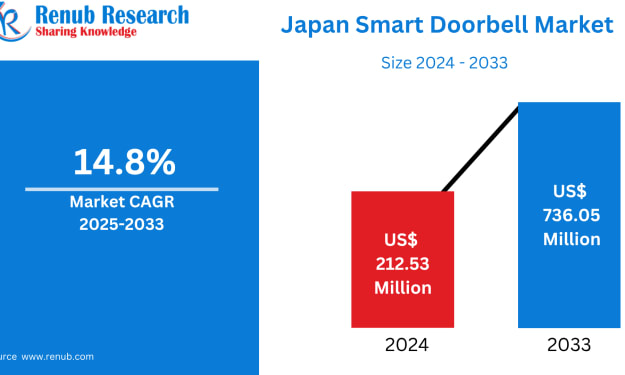

Japan Smart Doorbell Market Size and Forecast 2025–2033

Market Snapshot The Japan Smart Doorbell Market is expected to reach US$ 736.05 million by 2033, up from US$ 212.53 million in 2024, expanding at a robust CAGR of 14.8% from 2025 to 2033. Rapid urbanization, increasing adoption of smart home technologies, and rising demand for home security systems are driving market growth. Advancements in AI, video analytics, and wireless connectivity are further strengthening consumer demand for smart doorbell systems.

By Marthan Sir3 days ago in Futurism

How to Succeed at the Benson Directory®

Congratulations and welcome to the Benson Directory® employee #22391! As our newest call handler, you will have the privilege of speaking with dozens of unique and interesting people on a daily basis as well as the opportunity to earn bonuses for high performance. Contained within this handbook you will find a set of ease to follow instructions designed to help you settle in to your new role and begin paving the way to success.

By S. A. Crawford2 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.