High Purity Alumina Market Analysis: Electronics Growth, Supply Constraints & Forecast to 2034

How electric vehicle growth, energy storage investments, and advanced ceramics innovation are influencing production strategies in the high purity alumina market

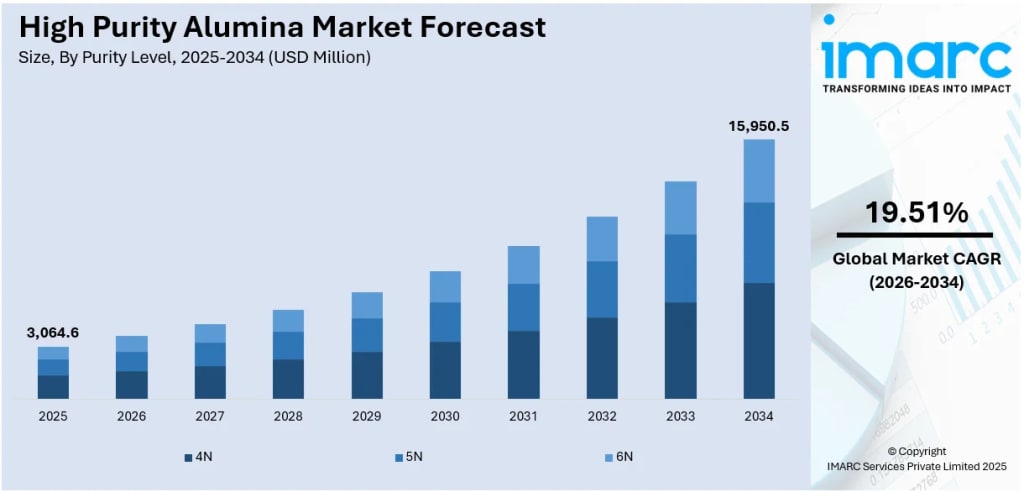

Rising demand from LED manufacturing, electric vehicle batteries, and advanced electronics is driving healthy market expansion, supported by technological innovations in production methods and growing adoption across semiconductor, sapphire substrate, and clean energy applications. According to IMARC Group’s latest data, the global high purity alumina market size was valued at USD 3,064.6 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 15,950.5 Million by 2034, exhibiting a CAGR of 19.51% from 2026-2034.

High purity alumina has become essential for next-generation technologies, with industries demanding ultra-pure materials for critical applications. The material’s exceptional thermal stability and chemical resistance make it indispensable for LED substrates, lithium-ion battery separators, and semiconductor components. Recent industry data shows that LED applications account for nearly half of global HPA consumption, while battery applications are experiencing explosive growth driven by the electric vehicle revolution.

High Purity Alumina Market Growth Drivers:

- Explosive Growth in Electric Vehicle Battery Production

Electric vehicle adoption is transforming the HPA landscape as manufacturers coat lithium-ion battery separators with high-purity alumina to enhance safety and performance. The International Energy Agency reported nearly 14 million electric cars sold globally, representing a 35% jump from previous levels. Battery makers are scaling up HPA-coated separator production to prevent thermal runaway and extend battery life. Chinese manufacturers dominate this space, with facilities in Guangdong and Jiangsu provinces ramping up output. Government subsidies for EV purchases in major markets continue to fuel battery demand, creating sustained HPA consumption growth.

- LED Lighting Transition Drives Substrate Demand

The global shift from traditional bulbs to LED technology is creating robust demand for sapphire substrates manufactured from high-purity alumina. The U.S. Department of Energy anticipates widespread LED installation completion, with ENERGY STAR-certified products using approximately 75% less energy than conventional lighting. Commercial building retrofits, street lighting upgrades, and residential adoption across developing economies are expanding the addressable market. Sapphire substrate production requires 4N-grade HPA for optimal crystal quality, with manufacturers in Taiwan and Japan leading innovation in larger wafer sizes and improved yields.

Receive Your Free High Purity Alumina Market Sample Report Now

- Semiconductor Industry Pushes Purity Requirements Higher

Advanced semiconductor manufacturing is driving demand for ultra-high purity alumina grades as chipmakers pursue smaller process nodes and improved performance. The CHIPS and Science Act positioned the United States to capture significant private investment, with over 90 new semiconductor projects announced across 28 states totaling nearly USD 450 billion. These facilities require HPA for substrate production and advanced packaging applications. Manufacturers are investing in hydrolysis processes capable of achieving 5N and 6N purity levels, with Australian and North American producers developing new capacity to serve domestic semiconductor fabs and reduce supply chain risks.

High Purity Alumina Market Trends:

- Low-Carbon Production Methods Gain Traction

Environmental concerns are pushing HPA producers toward sustainable manufacturing processes that dramatically reduce carbon emissions. Advanced Energy Minerals made significant progress producing low-emission high purity alumina at its Québec facility powered entirely by renewable energy, cutting CO₂ emissions from traditional levels of 12.3 tons per ton of HPA to nearly zero. Hydrochloric acid leaching and solvent extraction routes are emerging as energy-efficient alternatives to traditional methods. Australian developers are leveraging domestic renewable energy resources to build zero-carbon production facilities, appealing to environmentally conscious electronics manufacturers who are setting ambitious sustainability targets for their supply chains.

- Vertical Integration Reshapes Supply Chains

Major technology companies are securing HPA supply through strategic investments and partnerships to mitigate material shortages and price volatility. Battery manufacturers in South Korea and China are establishing direct relationships with HPA producers or developing in-house refining capabilities. Korea’s CIS Chemical secured investment from GENAXIS to expand its high-purity alumina production, targeting battery material markets with proprietary doping technology. LED manufacturers are similarly working backward into the supply chain. This integration trend is accelerating capacity announcements, with Alpha HPA’s Gladstone facility expected to become the world’s largest single-site HPA refinery, creating hundreds of local jobs and securing material for multiple customers.

- Advanced Applications Expand Beyond Traditional Markets

Innovation in medical bio-ceramics and specialized optical components is opening new avenues for HPA consumption beyond electronics and batteries. Manufacturers are developing ready-to-use bio-ceramic materials for orthopedic and dental implants, where HPA’s superior purity and biocompatibility offer distinct advantages. The optical components segment is growing as sapphire applications expand into smartphone camera lenses, luxury watch crystals, and aerospace windows. Impact Minerals secured a joint venture stake in Hipura for solvent extraction technology and pilot plant assets, positioning itself as Australia’s second-leading HPA producer. Chemical mechanical polishing applications for semiconductors are driving demand for specialized HPA formulations with precise particle size distributions.

Recent News and Developments in High Purity Alumina Market

- June 2025: Korea’s CIS Chemical secured investment from GENAXIS to expand its high-purity alumina and battery material production. Known for waste battery recycling and SSX technology, CIS Chemical plans factory expansion, new doping products, and global growth in semiconductors, displays, and rechargeable battery markets.

- May 2025: Andromeda Metals achieved a breakthrough by producing 99.9985% purity 4N High Purity Alumina using a cost-effective, low-carbon process. Backed by South Australia’s renewable energy, this positions Andromeda strongly in the growing global HPA market for semiconductors, LEDs, and batteries.

- April 2025: Impact Minerals secured a 50% joint venture stake in Hipura Proprietary Limited for USD 2.2 Million, acquiring solvent extraction technology and a nearly completed pilot plant. This accelerates Impact’s high-purity alumina production, positioning it as Australia’s second-leading HPA producer after Alpha HPA.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Andrew Sullivan

Hello, I’m Andrew Sullivan. I have over 9+ years of experience as a market research specialist.

Keep reading

More stories from Andrew Sullivan and writers in Futurism and other communities.

Dialysis Market Insights: Home Dialysis Expansion, Aging Population & Industry Outlook to 2034

Increasing prevalence of chronic kidney disease and end-stage renal disease, rising diabetes and hypertension cases, technological advancements in dialysis equipment, growing healthcare spending, expanding home dialysis solutions, and favorable government policies are driving robust market growth. The global dialysis market size was valued at USD 125.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 181.2 Billion by 2034, exhibiting a CAGR of 4.14% from 2026-2034.

By Andrew Sullivan2 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.