Global IV Bags Market Size and Forecast 2025–2033: Healthcare’s Silent Lifeline Expands Worldwide

Rising hospitalizations, safer materials, and home healthcare trends propel the IV bags industry into a new growth era

Global IV Bags Market at a Glance

The Global IV Bags Market is entering a period of sustained growth, driven by rising hospitalization rates, increasing surgical procedures, and the expanding need for safe, sterile, and efficient fluid delivery systems across healthcare settings. According to Renub Research, the global IV bags market is expected to grow from US$ 1.98 billion in 2024 to US$ 4.14 billion by 2033, registering a strong CAGR of 8.55% during 2025–2033.

Often overlooked but absolutely essential, IV bags form the backbone of modern medical treatment—delivering hydration, nutrients, medications, blood products, and life-saving therapies in hospitals, emergency rooms, clinics, and increasingly, in home-care environments. As healthcare systems evolve, the IV bag industry is quietly transforming alongside them.

Understanding the Role of IV Bags in Modern Medicine

IV bags are sterile containers used to deliver fluids and medications directly into a patient’s bloodstream through intravenous therapy. Made from materials such as polyvinyl chloride (PVC), polyethylene, polypropylene, and other advanced polymers, IV bags are fundamental to daily clinical operations.

From emergency care and surgeries to ICU management, chemotherapy, dialysis, and long-term chronic care, IV bags are universally used across all levels of healthcare. Their importance has only increased with rising chronic disease prevalence, aging populations, and the expansion of healthcare access in emerging economies.

As hospitals prioritize safety, efficiency, and sustainability, IV bag manufacturers are innovating rapidly—introducing safer materials, recyclable designs, and smarter packaging to meet global demand.

Key Growth Drivers Shaping the Global IV Bags Market

1. Rising Hospitalizations and Surgical Procedures Worldwide

One of the strongest drivers of IV bag demand is the continuous rise in hospital admissions. The world is experiencing a surge in chronic diseases, aging populations, and complex surgical interventions, all of which require intravenous therapy.

Globally, cardiovascular diseases alone cause around 18 million deaths annually, while cancer, respiratory disorders, and diabetes continue to rise. These conditions often require hospitalization and prolonged IV treatment, fueling consistent demand for IV bags.

Emerging economies are also investing heavily in hospital infrastructure, expanding access to inpatient care and emergency services—making IV bags a core medical consumable in global healthcare supply chains.

2. Transition to Non-PVC and Eco-Friendly IV Bags

Environmental and patient safety concerns are accelerating the shift away from traditional PVC IV bags. Plasticizers like DEHP, commonly used in PVC, have been linked to health risks, prompting regulatory bodies and hospitals to seek safer alternatives.

As a result, polyethylene and polypropylene IV bags are gaining momentum due to their non-toxic, DEHP-free, and recyclable properties. Regulatory encouragement from organizations like the FDA and EU REACH has further boosted adoption.

A notable example is Baxter International, which in December 2023 completed the first phase of its IV bag recycling program in the U.S., diverting over 6 tons of PVC IV bag waste from landfills—marking a major milestone in sustainable medical packaging.

3. Expansion of Home Healthcare and Ambulatory Services

The rapid expansion of home healthcare and ambulatory infusion services is reshaping IV bag demand. Patients increasingly receive hydration, nutrition, and drug therapy outside hospitals—especially in developed markets facing rising healthcare costs.

Portable, user-friendly IV bags are now essential for home infusion therapy, elderly care, and chronic disease management. This shift reduces hospital burden while improving patient comfort, driving new growth opportunities for IV bag manufacturers.

In December 2024, Endo Inc. launched the first FDA-approved premixed epinephrine IV bag, highlighting how innovation is supporting safer and faster IV therapy in both hospital and home-care settings.

Challenges Facing the Global IV Bags Market

1. Volatile Raw Material Prices

IV bag manufacturing relies heavily on petrochemical-derived polymers, making it sensitive to fluctuations in crude oil prices. Global supply chain disruptions and price instability directly impact production costs and profit margins, particularly for manufacturers in developing economies.

Managing long-term supply contracts and diversifying material sourcing has become crucial for maintaining affordability and consistent production.

2. Stringent Regulatory and Compliance Requirements

IV bags are classified as medical devices, meaning manufacturers must comply with strict safety and quality standards. Regulatory approvals from bodies such as the FDA, EMA, and ISO involve extensive testing, documentation, and audits.

While these regulations protect patients, they also increase development costs and delay product launches, especially for small and mid-sized manufacturers seeking global expansion.

Market Insights by Segment

Polyethylene IV Bags Market

Polyethylene IV bags are rapidly gaining market share due to their safety, clarity, and chemical stability. Being DEHP-free, they are ideal for sensitive applications such as oncology, pediatrics, and neonatal care.

Supportive regulations and growing hospital preference make polyethylene IV bags one of the fastest-growing segments, particularly in North America and Europe.

Polypropylene IV Bags Market

Polypropylene IV bags are valued for their high thermal resistance and inert nature, making them suitable for sterilization-intensive and long-term medication storage. Their lower leachability reduces drug interaction risks, which is critical in parenteral nutrition and specialty drug delivery.

Asia-Pacific and Europe are leading markets for polypropylene IV bags, driven by rising pharmaceutical innovation and regulatory emphasis on safer materials.

250–500 ml IV Bags Market

The 250–500 ml capacity segment is among the most commonly used sizes across healthcare settings. These bags offer the ideal balance between volume and handling convenience, making them suitable for hydration, drug delivery, and electrolyte therapy.

They are increasingly used in outpatient and home-care settings, contributing to steady volume growth across global markets.

Single Chamber IV Bags Market

Single chamber IV bags dominate the market due to their simplicity, affordability, and wide application. These bags are used extensively for hydration, antibiotics, and electrolyte therapy in hospitals, ambulatory centers, and emergency rooms.

Their versatility and cost-effectiveness make them especially popular in emerging economies, where standardization and affordability remain key priorities.

Regional Market Highlights

United States IV Bags Market

The U.S. remains one of the largest IV bag markets globally, supported by advanced healthcare infrastructure and high surgical volumes. There is a strong shift toward non-PVC, DEHP-free IV bags due to regulatory and patient safety concerns.

In July 2024, Amneal Pharmaceuticals received FDA approval for ready-to-use IV bags containing potassium phosphates, helping reduce compounding errors and improve hospital efficiency.

France IV Bags Market

France is a major contributor to the European IV bags market, driven by a robust public healthcare system and strong regulatory focus on sustainability. Hospitals are actively transitioning to non-PVC alternatives, aligning with EU environmental policies.

France is also investing in local production to reduce dependence on imports, strengthening domestic medical supply resilience.

India IV Bags Market

India’s IV bags market is growing rapidly due to healthcare expansion, rising medical tourism, and government initiatives like Ayushman Bharat. Increasing dialysis centers, cancer hospitals, and infection management facilities are boosting IV bag demand.

In June 2022, Gufic Biosciences introduced DEHP-free dual-chamber IV bags developed in collaboration with a French partner, reinforcing India’s move toward advanced, cost-effective medical consumables.

Mexico IV Bags Market

Mexico is emerging as a key IV bag manufacturing and export hub for North and Latin America. Investments in public healthcare infrastructure and rising chronic disease prevalence are fueling IV therapy demand.

The market is also transitioning toward safer, non-PVC alternatives, aligning with global standards.

Saudi Arabia IV Bags Market

Saudi Arabia’s IV bags market is expanding under Vision 2030, which emphasizes healthcare modernization and domestic manufacturing. Rising chronic diseases and hospital expansion projects are driving strong IV bag consumption.

Government support for local production is reducing import dependency and strengthening the country’s medical supply chain.

Global IV Bags Market Segmentation

By Material Type

Polyethylene

Polyvinyl Chloride (PVC)

Polypropylene

Other Material Types

By Capacity

0–250 ml

250–500 ml

500–1000 ml

By Chamber Type

Single Chamber

Multi Chamber

By Region

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Leading Companies in the Global IV Bags Market

Baxter International Inc.

Kraton Corporation

Technoflex

B. Braun Medical Inc.

Sippex IV Bags

Polycine GmbH

ICU Medical Inc.

Fresenius Kabi

Haemotronic

MedicoPack

Each company is analyzed based on overview, key persons, recent strategies, and financial insights, highlighting the competitive dynamics shaping the global market.

Final Thoughts

The Global IV Bags Market may not capture headlines, but it remains one of the most critical pillars of modern healthcare. As hospitals grow, home healthcare expands, and safety regulations tighten, IV bags are evolving from simple plastic containers into sophisticated, safer, and more sustainable medical devices.

With Renub Research forecasting the market to more than double by 2033, the industry is positioned for long-term, stable growth. Manufacturers that prioritize innovation, compliance, sustainability, and regional production will be best placed to lead this essential healthcare segment into the future.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in Futurism and other communities.

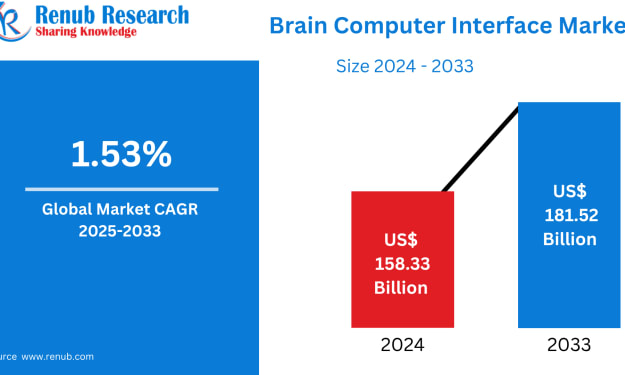

Global Brain Computer Interface Market Size & Forecast 2025–2033

Introduction: When the Human Brain Meets the Digital World The idea of controlling machines with the human mind once belonged strictly to science fiction. Today, that idea has become reality through Brain Computer Interface (BCI) technology—a revolutionary innovation that allows direct communication between the brain and external devices without the need for muscle movement or speech.

By Aaina Oberoi2 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight20 days ago in Futurism

How to Succeed at the Benson Directory®

Congratulations and welcome to the Benson Directory® employee #22391! As our newest call handler, you will have the privilege of speaking with dozens of unique and interesting people on a daily basis as well as the opportunity to earn bonuses for high performance. Contained within this handbook you will find a set of ease to follow instructions designed to help you settle in to your new role and begin paving the way to success.

By S. A. Crawford4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.