Fundus Camera Market Size & Forecast 2026–2034

AI-Driven Retinal Imaging and Preventive Eye Care to Redefine Global Ophthalmology

Introduction

The global healthcare landscape is witnessing a profound transformation driven by digital technologies, preventive care models, and an increasing focus on early diagnosis. Among the many diagnostic tools shaping modern ophthalmology, the fundus camera has emerged as one of the most critical instruments for detecting, monitoring, and managing retinal diseases. From diabetic retinopathy and glaucoma to macular degeneration and hypertensive retinopathy, fundus cameras play a central role in safeguarding vision and preventing avoidable blindness.

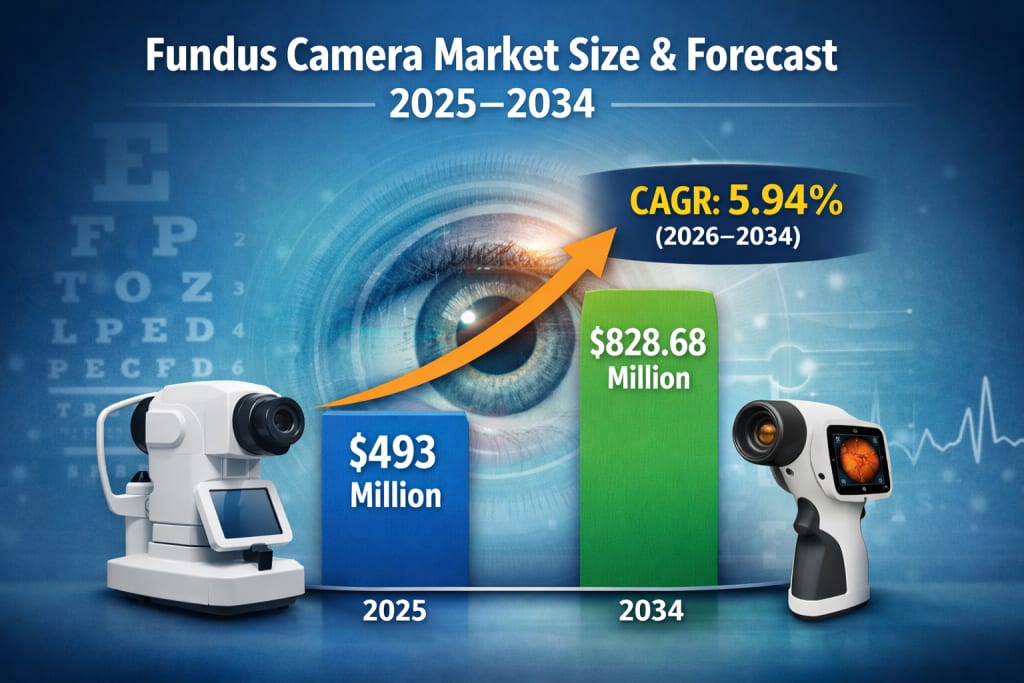

According to Renub Research, the Fundus Camera Market is projected to grow from US$ 493 million in 2025 to US$ 828.68 million by 2034, registering a compound annual growth rate (CAGR) of 5.94% during the forecast period 2026–2034. This steady expansion reflects not only the rising burden of eye diseases worldwide but also the growing adoption of preventive screening programs, teleophthalmology, and technologically advanced imaging systems such as non-mydriatic and AI-enabled fundus cameras.

As healthcare systems across the globe shift toward early detection and value-based care, the fundus camera is no longer confined to specialized eye hospitals. It is increasingly being used in primary care settings, community screening camps, mobile clinics, and telemedicine platforms—bringing retinal imaging closer to patients than ever before.

Fundus Camera Market Outlook

A fundus camera is a specialized medical imaging device designed to capture detailed photographs of the interior surface of the eye, known as the fundus. These images typically include the retina, optic disc, macula, and retinal blood vessels—structures that provide crucial insights into both ocular and systemic health conditions. Fundus photography has become an indispensable tool in diagnosing and monitoring diseases such as diabetic retinopathy, glaucoma, age-related macular degeneration (AMD), retinal vein occlusion, and hypertensive retinopathy.

Traditionally, fundus cameras were classified into mydriatic systems, which require pupil dilation, and non-mydriatic systems, which allow imaging without dilation and offer greater comfort and faster workflow. In recent years, the market has seen the introduction of hybrid devices, wide-field imaging systems, portable and handheld cameras, and AI-assisted platforms capable of automated disease detection.

Globally, adoption of fundus cameras has accelerated due to three major trends: the rising prevalence of diabetes and age-related eye diseases, the expansion of preventive screening programs, and the integration of digital health and teleophthalmology solutions. Governments and healthcare organizations are increasingly using fundus cameras in mass screening initiatives, particularly in remote and underserved regions, where access to ophthalmologists is limited. The combination of portability, digital connectivity, and cloud-based image sharing has significantly enhanced the reach and impact of retinal imaging technologies.

Growth Drivers of the Fundus Camera Market

Rising Prevalence of Eye Diseases and Chronic Conditions

One of the strongest drivers of the fundus camera market is the growing global burden of eye diseases linked to aging populations and lifestyle-related chronic conditions. The incidence of diabetic retinopathy, glaucoma, age-related macular degeneration, and hypertensive retinopathy continues to rise in parallel with increasing cases of diabetes and hypertension worldwide. These conditions often progress silently in their early stages, making regular retinal screening essential for timely diagnosis and treatment.

Fundus cameras enable clinicians to visualize the retina in detail, helping detect early pathological changes before patients experience noticeable vision loss. Early diagnosis not only improves clinical outcomes but also reduces long-term treatment costs, making fundus imaging an economically and medically valuable tool for healthcare systems.

According to global health estimates, billions of people are affected by near or distance vision impairment, with a significant proportion of cases being preventable or treatable if detected early. As populations age and life expectancy increases, age-related eye disorders are expected to become even more prevalent, further reinforcing the demand for reliable and efficient retinal imaging solutions.

Technological Advancements in Retinal Imaging

Continuous innovation in imaging technology is another major force propelling the fundus camera market forward. Modern fundus cameras offer higher image resolution, wider fields of view, faster image capture, and improved patient comfort compared to older systems. Non-mydriatic cameras, in particular, have transformed screening workflows by eliminating the need for pupil dilation, enabling faster examinations and higher patient throughput.

Digital imaging, cloud-based storage, and integration with electronic health records (EHR) have made it easier to store, share, and analyze retinal images across healthcare networks. Perhaps the most transformative development is the integration of artificial intelligence (AI) into fundus imaging systems. AI-powered algorithms can automatically detect signs of diabetic retinopathy, glaucoma, and other retinal pathologies, supporting clinicians in decision-making and improving diagnostic accuracy and efficiency.

Handheld and portable fundus cameras are also gaining popularity, especially in community screening programs, primary care clinics, and rural healthcare settings. These devices combine mobility with high-quality imaging, making retinal screening more accessible than ever before.

Expansion of Preventive Eye Screening and Teleophthalmology

The global shift toward preventive healthcare is significantly boosting the adoption of fundus cameras. Governments, non-profit organizations, and healthcare providers are increasingly implementing large-scale screening programs to identify eye diseases at an early stage, particularly among high-risk populations such as people with diabetes and the elderly.

Teleophthalmology has emerged as a powerful extension of these efforts. Retinal images captured in primary care centers, mobile clinics, or community camps can be transmitted to specialists in urban or tertiary care centers for expert evaluation. This model not only improves access to eye care in remote and underserved areas but also helps optimize specialist workloads and reduce healthcare disparities.

The combination of fundus cameras with telemedicine platforms is reshaping eye care delivery models, making retinal screening more scalable, efficient, and inclusive.

Challenges of the Fundus Camera Market

High Equipment Costs and Budget Constraints

Despite their clinical value, fundus cameras—especially advanced digital and wide-field systems—remain expensive. The high upfront cost of equipment, along with ongoing expenses for maintenance, software updates, and staff training, can be a significant barrier for small clinics and healthcare centers, particularly in low- and middle-income regions.

Public screening programs, which often operate under strict budget constraints, may also face difficulties in procuring high-end systems. While more affordable and portable models are gradually entering the market, cost sensitivity continues to limit broader adoption in resource-constrained settings.

Shortage of Skilled Professionals and Workflow Integration Issues

Effective use of fundus cameras requires trained personnel who can capture high-quality images and interpret results accurately. In many developing regions, there is a shortage of ophthalmologists, optometrists, and skilled technicians, which can limit the full utilization of these devices.

Additionally, integrating fundus cameras into existing clinical workflows and IT systems can be challenging. Issues such as resistance to new technologies, data management complexities, and interoperability with hospital information systems can slow down adoption, particularly in large or resource-limited healthcare facilities.

Market Segmentation Insights

Mydriatic Fundus Camera Market

Mydriatic fundus cameras continue to hold an important place in clinical settings where maximum image clarity and detailed retinal visualization are required. These systems, which involve pupil dilation, are widely used in hospitals and specialized ophthalmology clinics for comprehensive eye examinations and complex case evaluations. Although the dilation process can increase examination time and cause temporary patient discomfort, the superior image quality makes mydriatic cameras indispensable for detailed diagnostic work.

ROP Fundus Camera Market

The ROP (Retinopathy of Prematurity) fundus camera segment is focused on neonatal and pediatric care, particularly for screening premature and low-birth-weight infants. These specialized devices are used in neonatal intensive care units (NICUs) and pediatric ophthalmology clinics to detect early signs of retinal abnormalities. Growing awareness of early vision screening, rising premature birth rates, and advances in compact, wide-field imaging systems are driving demand in this niche but critical segment. Teleophthalmology integration further enhances access to expert consultation in neonatal care.

End-User Analysis

Fundus Camera Market in Ophthalmology Clinics

Ophthalmology clinics represent one of the largest end-user segments for fundus cameras. These clinics rely on retinal imaging for routine eye examinations, chronic disease management, and treatment planning. Non-mydriatic cameras are particularly popular in outpatient settings due to their speed, ease of use, and patient comfort. The compact design of modern systems also suits space-constrained clinics, supporting efficient workflows and high patient volumes.

Fundus Camera Market in Hospitals

Hospitals remain a key market for fundus cameras, especially for managing complex and multi-disciplinary cases. In addition to ophthalmology departments, fundus cameras are used in emergency units, neurology departments, and internal medicine wards to assess retinal changes associated with systemic diseases such as diabetes and hypertension. Hospitals typically prefer technologically advanced systems with high throughput, robust image management capabilities, and compatibility with electronic medical records. Teaching and research hospitals also use fundus cameras extensively for education and clinical studies.

Regional Market Perspectives

United States Fundus Camera Market

The United States is one of the largest and most technologically advanced markets for fundus cameras. High prevalence of diabetes, strong emphasis on preventive care, and supportive reimbursement policies drive widespread adoption across hospitals, clinics, and optometry practices. The U.S. market is also at the forefront of adopting non-mydriatic, wide-field, and AI-enabled fundus cameras, as well as teleophthalmology-based screening programs.

Germany Fundus Camera Market

Germany’s fundus camera market is characterized by a strong focus on diagnostic quality, patient safety, and evidence-based medicine. Hospitals and eye care centers use these devices extensively for managing diabetic retinopathy, glaucoma, and age-related eye diseases. While regulatory and cost-effectiveness considerations influence procurement decisions, the country’s well-organized healthcare system supports steady adoption of advanced imaging technologies and digital health solutions.

India Fundus Camera Market

India represents a high-growth market driven by a rapidly increasing burden of diabetes, hypertension, and preventable vision loss. Government-led screening programs, eye hospitals, and non-profit outreach initiatives are major users of fundus cameras, particularly portable and non-mydriatic models suited for high-volume and rural settings. Teleophthalmology plays a crucial role in extending specialist care to remote areas, making fundus cameras a cornerstone of India’s preventive eye care strategy.

Saudi Arabia Fundus Camera Market

Saudi Arabia’s market is driven by high healthcare investments, a strong focus on preventive medicine, and a high prevalence of diabetes. Hospitals and specialized eye care centers are increasingly adopting advanced fundus cameras, while telemedicine initiatives aim to improve access to specialist services in remote regions. Although smaller in volume compared to major Asia-Pacific markets, Saudi Arabia offers strong long-term growth potential due to sustained healthcare modernization efforts.

Market Segmentation

By Product Type:

Mydriatic Fundus Camera

Non-Mydriatic Fundus Camera

Hybrid Fundus Camera

ROP Fundus Camera

By End User:

Ophthalmic & Optometrist Offices

Ophthalmology Clinics

Hospitals

By Geography:

North America (United States, Canada)

Europe (France, Germany, Italy, Spain, United Kingdom, Belgium, Netherlands, Turkey)

Asia Pacific (China, Japan, India, Australia, South Korea, Thailand, Malaysia, Indonesia, New Zealand)

Latin America (Brazil, Mexico, Argentina)

Middle East & Africa (South Africa, Saudi Arabia, United Arab Emirates)

Competitive Landscape

The fundus camera market features several established and emerging players, each analyzed across five key viewpoints: Overview, Key Persons, Recent Developments & Strategies, Product Portfolio, and Financial Insights. Major companies operating in this space include:

Carl Zeiss Meditec AG

Topcon Medical Systems, Inc.

Merit Medical Systems, Inc.

NIDEK Co., Ltd.

Revenio Group

These companies continue to invest in innovation, AI integration, portability, and global expansion to strengthen their competitive positions.

Final Thoughts

The global fundus camera market is on a steady growth path, supported by rising rates of chronic eye diseases, expanding preventive screening programs, and rapid technological advancements in retinal imaging. With the market expected to grow from US$ 493 million in 2025 to US$ 828.68 million by 2034 at a CAGR of 5.94%, fundus cameras are set to remain a cornerstone of modern ophthalmic diagnostics.

As healthcare systems increasingly prioritize early detection, digital health, and equitable access to care, fundus cameras—especially portable, non-mydriatic, and AI-enabled models—will play an even more critical role in protecting vision worldwide. While challenges related to cost and workforce limitations remain, ongoing innovation and supportive public health initiatives are likely to ensure that retinal imaging becomes more accessible, efficient, and impactful in the years ahead.

About the Creator

Sakshi Sharma

Content Writer with 7+ years of experience crafting SEO-driven blogs, web copy & research reports. Skilled in creating engaging, audience-focused content across diverse industries.

Keep reading

More stories from Sakshi Sharma and writers in Futurism and other communities.

Europe SEO Market Size and Forecast 2026–2034

Introduction The Europe Search Engine Optimization (SEO) market is entering a decisive growth phase as businesses across industries prioritize organic visibility and long-term digital performance. According to Renub Research, the Europe SEO Market is expected to expand from US$ 19.02 Billion in 2025 to US$ 43.66 Billion by 2034, registering a strong CAGR of 9.67% during the forecast period 2026–2034.

By Sakshi Sharma2 days ago in Futurism

GCC Facility Management Market Analysis: Industry Overview, Key Players & Future Outlook

According to IMARC Group's latest research publication, GCC facility management market size reached USD 1.53 Billion in 2024. The market is projected to reach USD 3.44 Billion by 2033, exhibiting a growth rate (CAGR) of 8.70% during 2025-2033.

By Abhay Rajput5 days ago in Futurism

Industrial Ethernet Market: OT-IT Convergence & Next-Generation Factory Networks

Driven by Industry 4.0 adoption, IIoT integration, smart manufacturing investments, and rising demand for real-time, secure, high-speed industrial communication networks across automation-intensive industries. According to IMARC Group's latest research publication, global industrial ethernet market size reached USD 12.19 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 21.10 Billion by 2033, exhibiting a growth rate (CAGR) of 5.97% during 2025-2033.

By Andrew Sullivan4 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.