What Happens to an Abroad Education Loan if the Visa is Rejected?

Loan Effects due to Visa Rejection

For every Indian student dreaming of an international degree, the education loan is an essential step towards making that goal financially viable. However, what happens if you clear all hurdles, secure a sanctioned education loan, and then face the unexpected visa rejection?

It’s a scenario no one wants to think about, but being informed can help you pass through this curveball without financial or emotional setbacks. First things first, loan disbursement is usually tied to visa approval. In most cases, no funds are released until the visa is confirmed. That is a safeguard in place by both Banks and NBFCs to protect the borrower and the lender. If you are wondering what happens to an abroad education loan if the visa is rejected, well, this article has all the answers. Keep reading to find out more.

What Happens to an Abroad Education Loan if the Visa is Rejected after Sanction?

If your student visa is rejected and the education loan was only sanctioned but not disbursed, you owe the bank nothing, at least in most public sector cases. However, there are nuances to be aware of:

- Loan Cancellation: You will need to inform the lender about the visa rejection and officially request a cancellation of the sanctioned loan.

- Processing Fee Deductions: Some Private Banks or NBFCs may charge a non-refundable processing fee, ranging from INR 5,000 to INR 15,000. For example, HDFC Credila and Auxilo have non-refundable processing fees, while public banks like SBI and Canara Bank may refund the fee under certain circumstances.

- Interest Obligation: If any portion of the loan was disbursed before the visa result, e.g., to pay the University application fee, you will need to repay that amount with applicable interest.

What Happens to an Abroad Education Loan if the Visa is Rejected? Refund & Recovery

If no amount was disbursed, your liability ends with the cancellation process. But if funds were transferred, whether to the University or your account for pre-visa expenses, you will need to return those amounts.

In such cases, the lender will treat it like a short-term loan:

- You might be asked to repay immediately or

- The repayment might be structured into EMIs, depending on your repayment capacity.

NBFCs are stricter in recovery than Public Banks. It’s imperative to clarify your obligations during the loan agreement stage and ask for written documentation regarding disbursement and recovery terms post-visa rejection.

Impact on Credit Score & Future Student Loans for Studying Abroad

A cancelled education loan due to visa rejection doesn’t directly harm your credit score, particularly if the loan was not disbursed or was repaid promptly.

- If any disbursed amount is not repaid on time, it could reflect as a delay or default on your CIBIL report.

- If you reapply for another loan in the future, lenders may ask for clarification regarding the previous education loan. So, it’s smart to keep all communication with your bank documented and clean.

Honesty and timely communication with your lender protect your credit profile. Going forward, let’s have a quick glance at the different policies regarding student loans for studying abroad.

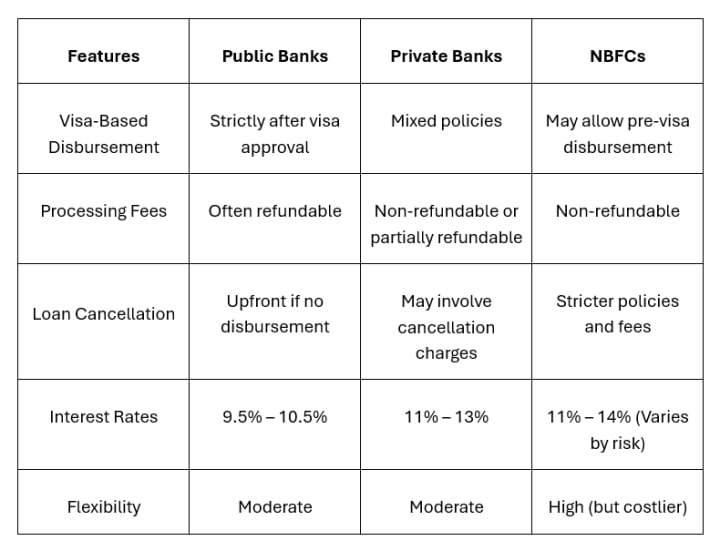

Lenders' Visa Rejection Policy Differences You Should Know

Some of the important policy differences that vary across different lenders are listed below:

Public sector banks are more conservative but also more student-friendly when it comes to loan cancellations post-visa rejection. Prevention is better than cure, so going ahead, let’s check some tips to reduce the hassles and risks.

Tips to Minimise Financial Risk Before Visa Approval

Being proactive is your best defence. Here is how to safeguard yourself beforehand:

- Choose Visa-Conditional Disbursement: Request your lender to add a clause that disbursement will only occur upon visa approval.

- Delay Disbursement: Don’t rush to take disbursements unless absolutely necessary, like paying a non-refundable university deposit.

- Clarify Cancellation Terms: Ask your lender upfront about what happens in the event of a visa rejection. Get this in writing.

- Pick the Right Lender: Compare policies of NBFCs, Private and Public Banks, not just interest rates, but for flexibility and recovery policies too.

- Maintain Backup Funds: Having a financial cushion can help cover pre-visa costs if recovery is required.

Visa rejection can feel like a crushing blow, but when it comes to your education loan, it doesn't have to wreck your finances or your future. By choosing the right lender, understanding their policies, and making informed decisions, you can protect yourself from unnecessary liabilities.

Always read the fine print and don’t hesitate to ask tough questions before signing that loan agreement. Reach out to an expert in an Overseas Education Loan Advisor to understand the criteria for an education loan better.

About the Creator

Riya Niar

I am dedicated professional counselor at ELAN Overseas Education Loan, specializing in assisting students with obtaining the best study abroad loan options. With a passion for helping students achieve their dreams of studying abroad.

How to Create Secure Passwords: Guide

Every day, millions of people log in to email accounts, social networks, banking apps, and work platforms without giving much thought to what protects their digital lives. The password, a simple string of characters, stands between personal data and potential intruders. Yet despite its importance, weak password practices remain one of the leading causes of account breaches worldwide.

By News Trends Go3 days ago in Education

Casie Hynes and the Future of Math Education Reform

Mathematics has always been a cornerstone of formal education. It strengthens reasoning, supports problem solving, and underpins critical fields such as science, technology, engineering, and economics. Yet despite its importance, math remains one of the most challenging subjects for students across the globe. Many learners struggle not because they lack ability, but because the way math is taught no longer aligns with how students learn or how the world now functions.

By Casie Hynes6 days ago in Education

Comments (1)

Nice article, those who wish to look for higher education abroad, this article is more informative. well explanation. Good luck.