Understanding Business Loans: How to Secure the Funding You Need

Navigating the Different Types and Requirements of Business Financing

Starting a business can be a daunting task, especially when it comes to securing the necessary funding to get it off the ground. Business loans can be a great way to get the financing you need to grow and expand your business, but it can be difficult to know where to start. In this article, we will explore the different types of business loans available and the requirements needed to secure them.

First, it is important to understand the difference between secured and unsecured business loans. A secured loan requires the borrower to pledge collateral, such as property or equipment, in order to secure the loan. An unsecured loan, on the other hand, does not require any collateral and is based on the creditworthiness of the borrower. Secured loans typically have lower interest rates and longer repayment terms than unsecured loans, but they also come with a higher risk of losing the collateral in case of default.

The most common types of business loans include:

Small Business Administration (SBA) loans: These loans are backed by the government and are designed to help small businesses access funding. SBA loans can be used for a variety of purposes, such as starting or expanding a business, purchasing equipment or real estate, or working capital.

Traditional bank loans: These loans are offered by commercial banks and credit unions. They typically have longer repayment terms and lower interest rates than other types of loans, but they also have stricter qualifications and require a strong credit history.

Merchant cash advances: These loans are based on the future sales of a business and are typically used for working capital or inventory. They are often easier to qualify for than traditional bank loans, but they also have higher interest rates.

Online lenders: These lenders offer a variety of loan products, including short-term loans, line of credit, and invoice financing. They often have less stringent requirements than traditional banks, but they also have higher interest rates.

To secure a business loan, you will typically need to provide financial statements, tax returns, and a business plan. You will also need to have a good credit history and a solid business plan that demonstrates how you plan to use the loan to grow and expand your business.

In conclusion, business loans can be a great way to get the funding you need to start or expand your business. However, it is important to understand the different types of loans available and the requirements needed to secure them. By doing your research and understanding the pros and cons of each type of loan, you can find the best option for your business.

Another important factor to consider when applying for a business loan is the interest rate. The interest rate is the percentage of the loan that you will have to pay back in addition to the principal amount. Different types of loans have different interest rates, with secured loans typically having lower rates than unsecured loans. It's important to compare the interest rates of different loan options to ensure you are getting the best deal possible for your business.

Another important aspect to consider when applying for a business loan is the repayment terms. The repayment terms refer to the length of time you have to pay back the loan, as well as the schedule of payments. Different types of loans have different repayment terms, with traditional bank loans typically having longer terms than online loans. It's important to choose a loan with terms that you can comfortably afford to repay so you don't fall behind on payments.

One of the most important things to remember when applying for a business loan is to be prepared. This means having all of the necessary documentation and information ready to go. This includes financial statements, tax returns, and a business plan. You will also need to have a good credit history, as this will greatly impact your chances of getting approved for a loan.

It's also important to remember that there are many resources available to help you navigate the process of applying for a business loan. The Small Business Administration (SBA) is a great place to start, as they offer a wide range of loan programs and resources to help small business owners. Additionally, many banks and credit unions offer business lending services and can provide guidance on the loan application process.

In conclusion, business loans can be a great way to get the funding you need to start or expand your business. However, it's important to understand the different types of loans available, the requirements needed to secure them, and the terms and conditions of repayment. By doing your research, being prepared, and reaching out to resources such as the SBA, you can find the right loan for your business and secure the funding you need to succeed.

About the Creator

Keep reading

More stories from Muthukumar Baskaran and writers in Education and other communities.

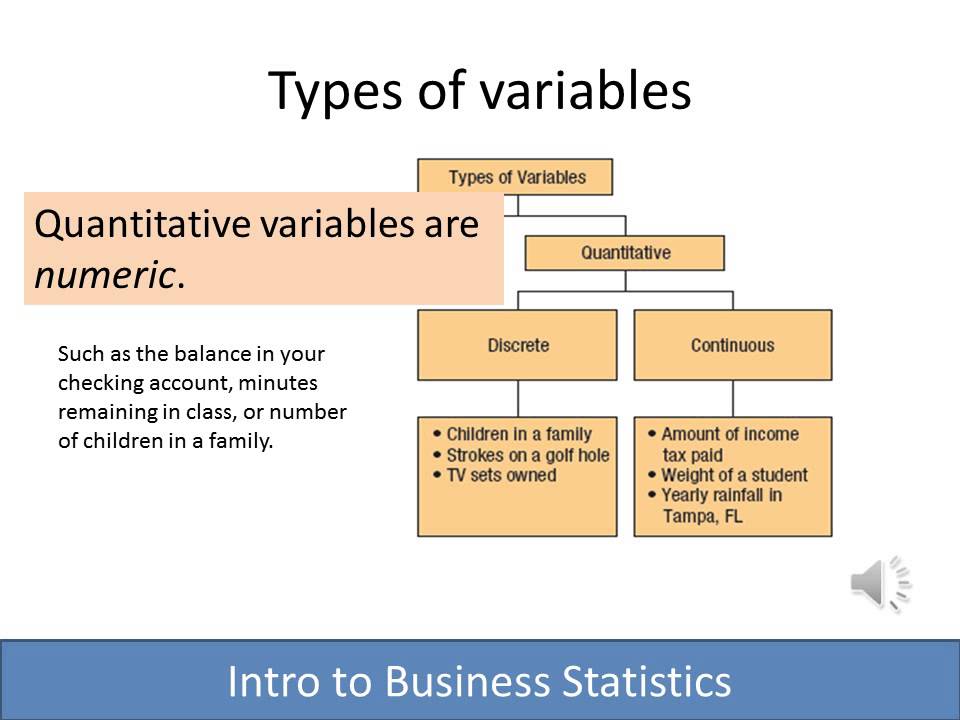

Understanding Business Statistics: A Guide for Entrepreneurs

As an entrepreneur, you are constantly making decisions that can impact the success of your business. Whether it's deciding on a new product to launch or figuring out the best way to market your services, it's essential to have a good understanding of the data and statistics that can inform these choices.

By Muthukumar Baskaran3 years ago in Education

A brief history of alcohol

This chimpanzee stumbles across a windfall of overripe plums. Many of them have split open, drawing him to their intoxicating fruity odor. He gorges himself and begins to experience some… strange effects. This unwitting ape has stumbled on a process that humans will eventually harness to create beer, wine, and other alcoholic drinks. The sugars in overripe fruit attract microscopic organisms known as yeasts. As the yeasts feed on the fruit sugars they produce a compound called ethanol— the type of alcohol in alcoholic beverages.

By Munesh Yadav24 minutes ago in Education

The Lean Advantage: How Small Improvements Create Massive Business Wins

In today’s fast-moving market, businesses don’t always need massive overhauls to see major growth. The real competitive advantage often comes from Lean process improvement—small, consistent changes that reduce waste, improve speed, and strengthen customer value. With a proactive approach, companies can spot inefficiencies early, prevent recurring problems, and build smarter systems before minor issues become costly setbacks.

By Duke Valentoura day ago in Education

Comments

There are no comments for this story

Be the first to respond and start the conversation.