Production economics

"The Evolution and Significance of Production Economics: From Adam Smith to the Knowledge-Based Economy".

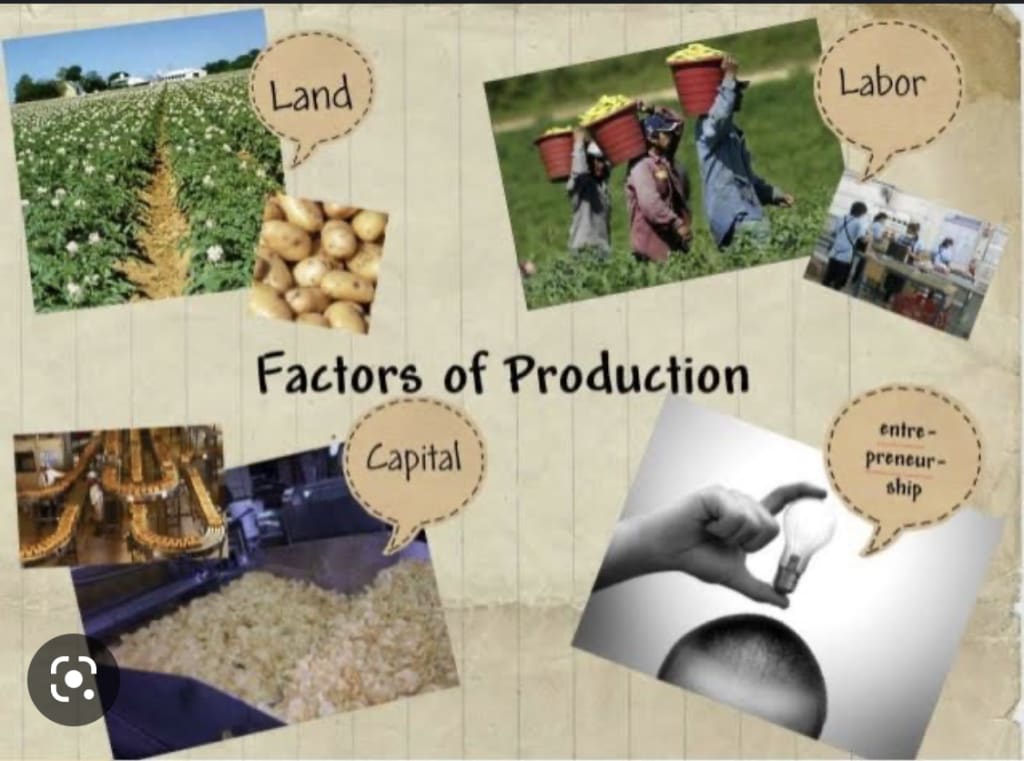

Production economics is the branch of economics that studies the production process and the efficient allocation of resources to produce goods and services. Its origins can be traced back to the classical economists, who first examined the factors of production and how they could be combined to create output.

One of the early contributions to production economics was made by Adam Smith, who in his seminal work "The Wealth of Nations" argued that the division of labor was the key to increased productivity. He believed that by breaking down the production process into smaller, specialized tasks, workers could become more efficient and productive.

In the 19th century, the Industrial Revolution transformed the way goods were produced. This led to the emergence of new concepts in production economics, such as economies of scale and the use of technology to increase productivity.

The late 19th and early 20th centuries saw the development of the neoclassical approach to production economics, which emphasized the role of prices and markets in determining the optimal allocation of resources. This approach focused on the efficient use of inputs such as labor, capital, and natural resources to maximize output.

In the mid-20th century, a new approach called the "production function" was introduced, which mathematically modeled the relationship between inputs and output. This approach allowed for more precise analysis of production processes and led to the development of theories such as the Cobb-Douglas production function.

More recent developments in production economics have focused on the role of innovation and technology in the production process. This includes the study of knowledge-based economies, where ideas and innovation are the key drivers of economic growth.

Overall, production economics has evolved significantly over time, from the early classical theories to the more recent emphasis on technology and innovation. Its central goal remains the same, however, which is to ensure that resources are allocated efficiently to produce goods and services that meet the needs of society.In addition to the neoclassical and production function approaches, another important development in production economics was the introduction of the concept of "transaction costs" by Ronald Coase in his 1937 paper "The Nature of the Firm." Coase argued that the existence of firms could be explained by the fact that certain transactions, such as hiring workers or buying inputs, can be conducted more efficiently within a firm than in the market.

This led to the development of the field of transaction cost economics, which focuses on the costs associated with exchanging goods and services, and how firms and markets can be designed to minimize those costs.

Another key concept in production economics is the idea of "efficiency." Economists study efficiency in production in terms of technical efficiency, which measures the amount of output that can be produced from a given set of inputs, and allocative efficiency, which measures the degree to which resources are allocated to their most productive use.

Efficiency is an important consideration for firms, as it directly affects their profitability. Firms that can produce goods and services at lower cost are able to offer lower prices and/or higher quality products, giving them a competitive advantage in the marketplace.

Overall, production economics plays a crucial role in shaping our understanding of how goods and services are produced, and how resources can be allocated efficiently to meet the needs of society. It is a dynamic field that continues to evolve and adapt to new challenges, such as the increasing importance of technology and innovation in the production process.In addition, production economics is closely related to other fields such as industrial organization, supply chain management, and operations research, which provide further insights into the production process. By studying production economics, economists can help firms and policymakers make informed decisions about how to allocate resources and increase productivity, ultimately leading to greater economic growth and prosperity.

About the Creator

Abdul Rehman

M.Phil(Hons) Agri Economics

Keep reading

More stories from Abdul Rehman and writers in Education and other communities.

Redefining the Deal: How Modern Private Equity Is Building Sustainable Success

Private equity has long relied on proven playbooks, disciplined capital deployment, and patient timelines. For decades, these fundamentals delivered consistent returns and shaped a powerful asset class. However, markets no longer behave the way they once did. Economic cycles move faster, competition intensifies, and information flows instantly. As a result, private equity firms now face pressure to evolve while preserving the strengths that built their reputations. Modern success depends on adaptation, agility, and a sharper understanding of value creation.

By Michael Christopher Venturino7 days ago in Education

Killing him slowly

There’s an intruder in my house again. He stumbles through the door, wet carrier bags in hand. He’s bought me offerings. I show my appreciation, letting him caress my beautiful body. He wants to touch me. I rub myself against his legs. He sighs, dropping the bags. He can’t resist touching me. Running his hand slowly down my spine, I arch my back towards his caress, let out a low purr. It’s what we both need.

By N J Delmas4 days ago in Horror

Comments

There are no comments for this story

Be the first to respond and start the conversation.