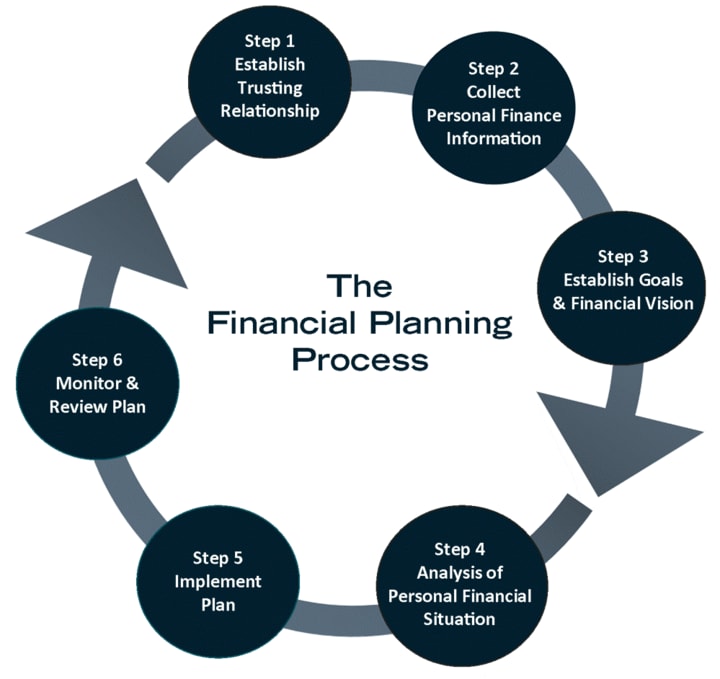

A Step-by-Step Guide to Building a Personal Financial Plan

Here's a step-by-step guide to building a personal financial plan

BY JAMES S. T. FONG "A Personal financial planning is an important process of considering one’s entire financial commitment and is critical for every person."

When it comes to handling money in the today’s world so fast, where are we and can we have hoped for that financial stability for the personal financial security? But if you have a clear personal finance plan what you will be able to do is have control over your money, achieve your objectives and plans, and build your future. The mentioned financial plan is not only for the financially affluent, but it is a cornerstone to make wealth and overcome financial hardship for anyone in the society.

Below is a guide that will help you develop your own successful personal financial plan.

1. Check Your Current Status

The first step in goal setting for anyone is always to have a financial snapshot to determine one’s baseline. The basic step is assessing your financial condition through data about your income and expenditure, outstanding loans, and the property owned. List out your:

Monthly income from all sort of sources whether it may be salary, investments, part time job etc.

Rent, utilities and regular interests on loans are consider fixed expenses.

Expenses whose amounts vary with the level of activity for a specific account (Meier & Sanker, 2012) (food costs, leisure, transportation).

Accounts payables (students loans, credit card balances, mortgages).

Money (cash, checks, bonds, savings accounts, mutual funds, stocks, property, pensions).

From this financial picture you will obtain a crisp vision of the present financial situation of your cash and net value. Once you’re armed with this knowledge, you can feel comfortable and charged up planning your financial future.

2. Set Clear Financial Goals

A financial aim is very important when it comes to any kind of financial planning. Your goals should be clear, quantifiable, attainable, relevant and timely based (SMART). Depending on the schedule of investment, they could be classified as or short-term investments that are expected to be held for a year or less, medium term investment that may take 1- 5 years and long-term investments that take 5 years and above. Here are some examples of goals:

Short-term: Set up an emergency fund with thrice to six times the amount of your average expenses per month.

Medium-term: High interest credits should be cleared as they attract very high charges such as credits cards.

Long-term: For things like retirement, purchasing a house or for children’s college expenses.

They suggest writing out your goals and ranking them. For example, establishing an emergency fund may occur before the development of a vacation fund of a car fund.

3. Create a Budget

A budget is one of the simplest principles of managing your money. Overall, it provides checks previous that one is using less money than they are earning and can channel resources towards fulfilling that budget. To create a budget, follow these steps:

Track your income and expenses: If you have not done so, then begin to find ways of tracking your income and expenses for loop holes on spending.

Differentiate between needs and wants: Remember always prioritize and cater for your needs such as rent, electricity, water, food and fare in getting to work before doing otherwise.

Assign spending limits: Follow this budgetary Glide: ‘50-30-20’, thirty percent of your earnings go to necessities, 30% to the things you desire and the rest 20% to saving or paying your loans.

Review and adjust: Ensure a periodic check on your budget then make necessary changes probably due to drooping or increased incomines or unexpected expenses.

Budgeting enables you to live within your income level and provides the free income required for achieving the financial goals.

4. Build an Emergency Fund

It is always important for any financially strategic plan to include an emergency fund. Emergency funds facilitate individuals when they experience financially pressing situations like, medical bills, loss of a job or house hold emergencies. Ideally, to have a fully funded emergency fund, you should have money equal to up to six months of your living expenses saved within an easily accessible savings account with reasonable return, like a high yield savings account.

If you have to, start contributing a little each month, but the thought is to consistently chip in and allow your money to grow over time. It thus means that with an emergency fund, you will be relieved, and more importantly, you will not be plunged into debts any time you have an emergency.

5. Manage and Pay Off Debt

It is worth stating that debt may be a real obstacle on the way to the economic freedom. To begin, write down all your obligations for credit cards, educational loans, auto loans, mortgages and the likes. Especially be wary of the suitable interest rates and manage those debts that are costly in the long run, in the first place.

Here are two common strategies for paying off debt:

Debt snowball method: Major on reducing on the smaller debts first then gradually move to the next until you are through.

Debt avalanche method: Contribute money to the visa with the highest interest rate, meaning the most money will be saved in the long term.

They are both good so choose the one that you feel best fits your circumstance.

6. Invest for the Future

Saving is not the only path for increasing wealth but investing is one of the most effective techniques. The first step is to participate in the company sponsored retirement scheme like the 401(k) and try to match existing contributions. If your employer does not offer a retirement plan, or the details of the plan are not satisfactory, you should open an Individual Retirement Account (IRA).

However, there are other investment products that one can invest in such as mutual investment funds, stocks, shares, bonds, real estate and many others depending on one’s risk taking abilities or the investment objectives admired. Defending yourself from the volatile swings and increasing future returns is possible if you choose diversified investments.

Please do not forget that investing is a long-term business despite the high volatility in the markets. It also helps the more you begin to invest early the more time your money has to compound and yield more.

7. Avoid the Mistakes and Check Your Financial Plan Frequently

This means your financial needs and forecasts will be subject to change based on factors such as marriage, children or job shift. That’s why one of the most important rules of good financial planning is to revise your plan from time to time. Keep a meeting to review your financial plan on a yearly basis in order to know how well you are performing and which aspect need correction.

Ask yourself:

Do you save enough money as you planned?

Have your priorities changed?

Have there been any income changes in your home that require you to shift some of your budgetary plans?

Thus, the goals of saving and investing should stay flexible and it is quite beneficial to go back to the plan from time to time.

Conclusion

Personalising one’s financial plan is a long-term activity that should be guided by some certain strategy and regularity. Evaluating your current financial position, determining your needs, overcoming excessive spending, minimizing and correctly disposing of a loan, and efficient investing allow you to become financially stable and lead a less_. From a financial plan you will be able to make regular reviews and adjustments that will make the financial planning suits the changing needs and goals that you have of your financial future.

FOLLOW FOR MORE..... increase the financial growth

About the Creator

Alak

A writer comps thoughts into stories from where characters wake up to life. Each line create a bridge between the imaginative world and the actual world.

Was Alexander the great really that great?

Order, order! Who do we have on the stand today? Alexander... the Great, eh? Well, what’s so great about him? Your honor, the better question is, what's not great about him? He was the King of Macedon and considered a living demigod by Egyptians and Greeks alike. He conquered Persia when it was one of Earth's largest empires. And he was a thoughtful student of Aristotle, creative enough to untie the impossibly tight Gordian knot by cutting it in half. The Gordian knot is a myth— just like the countless other stories invented to enhance Alexander’s legend!

By Munesh Yadav3 days ago in Education

Preparing Health Systems to Perform Under High-Stakes Crisis Conditions

High-stakes crises have become an increasingly common challenge for health systems worldwide. Whether dealing with infectious disease outbreaks, natural disasters, mass casualty incidents, or cybersecurity breaches, healthcare organizations must be ready to respond rapidly and effectively. Preparation is essential not only to ensure patient safety but also to maintain operational stability during times of extreme pressure. Health systems that invest in proactive planning, strong leadership, and resilient infrastructure are better equipped to manage crises without compromising care quality. Preparing for high-stakes situations requires a comprehensive approach that focuses on readiness, coordination, and continuous learning.

By Craig Kenta day ago in Education

The CEO of Everything

They say "jack of all trades, master of none," but they forgot to mention the part where the jack of all trades is also the camera woman, the makeup artist, and the person currently yelling at a tangled Wii microphone cable in a her own bathroom while recording herself singing and trying to make it look realistic and professional. (As professional as you can make it with nothing but a cell phone camera and a mic that doesn't work)

By Sara Wilson5 days ago in Humans

Comments

There are no comments for this story

Be the first to respond and start the conversation.