Global Polyethylene Market Size and Forecast 2025–2033: Growth Driven by Packaging, Infrastructure, and Sustainable Innovation

Rising Demand for Lightweight, Affordable Materials Fuels Steady Market Expansion Worldwide

Introduction

Polyethylene, the world’s most widely produced plastic polymer, continues to play a crucial role in modern industrial and consumer economies. From food packaging and construction materials to agricultural films and automotive components, polyethylene is deeply embedded in everyday life. Its lightweight nature, durability, versatility, and cost-effectiveness make it indispensable across numerous industries.

According to Renub Research, the global polyethylene market is expected to grow from US$ 154.22 billion in 2024 to US$ 201.57 billion by 2033, registering a CAGR of 3.02% from 2025 to 2033. This steady growth reflects rising demand from end-use industries, continuous technological improvements, and increasing investments in recycling and sustainable production.

Despite regulatory pressure and environmental concerns, polyethylene remains essential to global manufacturing and trade. Innovations in materials science, recycling technologies, and bio-based feedstocks are reshaping the industry, ensuring that polyethylene continues to evolve alongside sustainability goals.

Global Polyethylene Market Overview

Polyethylene is a thermoplastic polymer primarily derived from ethylene, which is produced from natural gas and crude oil. The material is available in several grades, including:

Low-Density Polyethylene (LDPE) – flexible and widely used in films and bags

Linear Low-Density Polyethylene (LLDPE) – strong and stretchable, ideal for packaging

High-Density Polyethylene (HDPE) – rigid, durable, and used in pipes, containers, and construction

The packaging industry remains the dominant consumer of polyethylene, accounting for a large portion of global demand. With the growth of urbanization, e-commerce, and modern retail, demand for safe, lightweight, and protective packaging solutions continues to increase. Polyethylene’s moisture resistance, flexibility, and low cost make it a preferred material for both manufacturers and consumers.

At the same time, emerging economies in Asia-Pacific and the Middle East are expanding production capacity, strengthening global supply chains and boosting exports. Integrated petrochemical complexes and access to low-cost feedstocks have enabled major producers to achieve scale efficiencies, further reinforcing polyethylene’s market leadership.

Key Factors Driving Polyethylene Market Growth

1. Rising Demand from the Packaging Industry

Packaging is the backbone of polyethylene consumption worldwide. The rapid growth of packaged food, beverages, pharmaceuticals, and personal care products has significantly increased demand for polyethylene films, bottles, containers, and pouches. The material’s ability to preserve freshness, protect products, and extend shelf life makes it indispensable for modern packaging.

E-commerce has further accelerated this demand, as protective and lightweight packaging is essential for logistics efficiency. Additionally, innovations such as multilayer films, recyclable mono-material packaging, and high-performance polyethylene grades are expanding application possibilities.

In emerging economies, the expansion of the fast-moving consumer goods (FMCG) sector continues to boost packaging demand, reinforcing polyethylene’s long-term growth outlook.

2. Infrastructure Development and Construction Expansion

Infrastructure development is another major driver of polyethylene demand. HDPE, in particular, is widely used in water supply systems, gas distribution networks, telecom ducts, geomembranes, and insulation materials. Its resistance to corrosion, flexibility, and long lifespan make it ideal for large-scale infrastructure projects.

Governments across Asia, Africa, and the Middle East are investing heavily in urban infrastructure, smart cities, and transportation networks. As older systems are replaced with modern, efficient alternatives, polyethylene-based solutions are increasingly favored due to lower maintenance costs and durability.

Green building initiatives and sustainable construction practices further support polyethylene’s adoption in the construction sector.

3. Technological Innovation and Product Development

Technological advancements have significantly enhanced polyethylene performance and application scope. Modern catalyst technologies, such as metallocene catalysts, allow manufacturers to create stronger, thinner, and more flexible materials with improved mechanical properties.

Additionally, the industry is investing in bio-based polyethylene derived from renewable feedstocks like sugarcane, helping reduce carbon footprints. Chemical recycling and advanced mechanical recycling technologies are also improving material recovery and reuse, supporting circular economy models.

These innovations not only improve environmental performance but also enable polyethylene to compete with alternative materials in high-value applications such as medical devices and specialty packaging.

Challenges Facing the Polyethylene Market

1. Environmental and Regulatory Pressure

Environmental concerns surrounding plastic waste have become one of the biggest challenges for the polyethylene industry. Governments worldwide are implementing strict regulations, including bans on single-use plastics, mandatory recycled content requirements, and extended producer responsibility (EPR) policies.

Public perception of plastic pollution is also influencing consumer behavior, prompting brands to seek sustainable packaging alternatives. As a result, manufacturers are being forced to invest heavily in recycling infrastructure, material innovation, and compliance systems.

While these regulations may slow demand in certain segments, they also create new opportunities for recycled and bio-based polyethylene products.

2. Raw Material Price Volatility

Polyethylene production depends heavily on ethylene, a byproduct of oil and natural gas processing. Fluctuations in crude oil prices, geopolitical tensions, supply chain disruptions, and OPEC production decisions can significantly affect production costs and profitability.

This volatility creates challenges in pricing strategies, cost forecasting, and long-term investment planning. Additionally, transitioning to alternative feedstocks or renewable inputs often requires higher capital investments, adding complexity to production decisions.

Polyethylene Market Overview by Region

United States Polyethylene Market

The United States remains one of the most competitive polyethylene producers globally, supported by abundant shale gas resources and advanced petrochemical infrastructure. The country is a major exporter, supplying polyethylene to global markets due to its cost-efficient ethylene production.

Domestic demand is driven by packaging, construction, automotive, and consumer goods industries. Investments in recycling facilities and circular economy initiatives are reshaping market dynamics, while sustainability commitments are encouraging the use of recycled polyethylene in packaging.

Major companies such as Dow, ExxonMobil, and LyondellBasell continue to invest in capacity expansion and innovation, strengthening the U.S. market’s long-term outlook.

United Kingdom Polyethylene Market

In the United Kingdom, polyethylene demand is influenced by strict environmental regulations and sustainability policies. The Plastic Packaging Tax and recycling mandates have accelerated the adoption of recycled and bio-based materials.

Although domestic production has declined, imports continue to meet market demand across packaging, construction, and agriculture. Companies are actively investing in circular economy initiatives to meet regulatory requirements and consumer expectations.

Despite supply chain challenges following Brexit, innovation and regulatory support continue to sustain market stability.

India Polyethylene Market

India is one of the fastest-growing polyethylene markets, driven by urbanization, rising incomes, and infrastructure development. Packaging remains the largest application, followed by construction, agriculture, and automotive uses.

Government initiatives such as Make in India and the Smart Cities Mission are fueling demand for HDPE pipes and construction materials. Domestic producers like Reliance Industries and Indian Oil Corporation are expanding capacity to meet rising demand.

While environmental regulations are evolving, India’s strong informal recycling sector continues to play a key role in polyethylene reuse. Growing investments in petrochemical infrastructure position India as a major growth hub for the global market.

United Arab Emirates Polyethylene Market

The UAE benefits from easy access to low-cost feedstocks, world-class petrochemical infrastructure, and strong export connectivity. Polyethylene production is closely aligned with the country’s industrial diversification strategy under Vision 2030.

Companies like Borouge are expanding capacity and developing advanced polyethylene grades for domestic and international markets. Packaging, construction, and industrial applications dominate domestic consumption.

Although environmental regulations are less strict than in Europe, rising global sustainability expectations are encouraging investment in recycling and cleaner production technologies.

Recent Industry Development

November 2023:

NOVA Chemicals Corporation signed a Memorandum of Understanding (MoU) with Amcor to supply mechanically recycled polyethylene. This partnership highlights the industry’s growing focus on circular economy solutions and sustainable packaging materials.

Market Segmentation

By Product Type

Low-Density Polyethylene (LDPE)

High-Density Polyethylene (HDPE)

Linear Low-Density Polyethylene (LLDPE)

By Application

Bottles & Containers

Films & Sheets

Bags & Sacks

Pipes & Fittings

Other Applications

By End Use

Packaging

Construction

Automotive

Agriculture

Consumer Electronics

Other End Uses

By Region

North America: United States, Canada

Europe: France, Germany, Italy, Spain, United Kingdom, Belgium, Netherlands, Turkey

Asia Pacific: China, Japan, India, South Korea, Thailand, Malaysia, Indonesia, Australia, New Zealand

Latin America: Brazil, Mexico, Argentina

Middle East & Africa: Saudi Arabia, United Arab Emirates, South Africa

Key Players Covered in the Market

BASF SE

Borealis AG

Braskem

Exxon Mobil Corporation

Formosa Plastics

INEOS Group

LG Chem

LyondellBasell Industries Holdings B.V.

MOL Group

Mitsubishi Chemical Corporation

Each company is analyzed based on company overview, key personnel, recent developments, SWOT analysis, revenue analysis, and strategic positioning.

Final Thoughts

The global polyethylene market is entering a phase of stable and sustainable growth. While environmental regulations and raw material price volatility pose challenges, rising demand from packaging, infrastructure, and emerging economies continues to support expansion.

With the market projected to reach US$ 201.57 billion by 2033, manufacturers that invest in recycling technologies, sustainable materials, and advanced production processes will be best positioned to thrive in the coming decade. As the industry evolves toward a circular economy, polyethylene will remain a foundational material—adaptable, innovative, and essential to global development.

About the Creator

Marthan Sir

Educator with 30+ years of teaching experience | Passionate about sharing knowledge, life lessons & insights | Writing to inspire, inform, and empower readers.

Keep reading

More stories from Marthan Sir and writers in Earth and other communities.

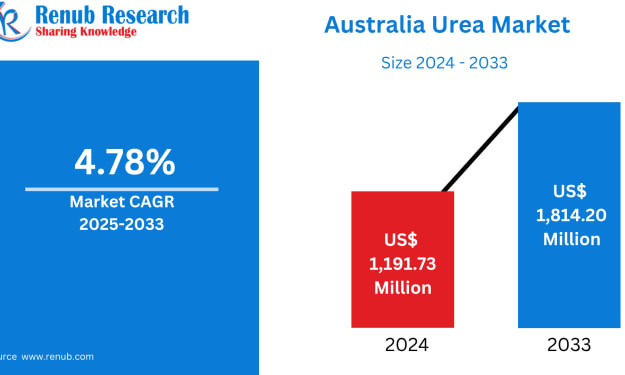

Australia Urea Market Size and Forecast 2025–2033

Australia Urea Market Overview The Australian Urea Market is anticipated to reach US$ 1,814.20 million in 2033, up from US$ 1,191.73 million in 2024, growing at a CAGR of 4.78% during 2025–2033, according to Renub Research. This growth is being driven by increasing demand from the agricultural sector for high-nitrogen fertilizers, expanding grain and crop cultivation, and rising government incentives for sustainable farming practices. Import substitution policies and growing interest in domestic production capabilities are also shaping market dynamics.

By Marthan Sir3 days ago in Earth

"NASA satellites confirm that China’s Great Green Wall is effectively slowing desert expansion and reshaping entire regions

NASA satellite data has confirmed what scientists, policymakers, and local communities in China have hoped for decades: the Great Green Wall is working. Designed to slow the relentless expansion of deserts across northern China, this ambitious ecological project is not only reducing desertification but also reshaping entire regions—environmentally, economically, and socially. Often compared to Africa’s Great Green Wall, China’s version is one of the largest environmental engineering projects in human history. Officially known as the Three-North Shelter Forest Program, it stretches across northern, northeastern, and northwestern China, covering an area larger than many countries. Launched in 1978, the project aims to combat desert expansion, reduce sandstorms, protect farmland, and stabilize local climates through large-scale tree planting and vegetation restoration. For years, critics questioned whether planting trees in arid and semi-arid regions was sustainable. Some argued that trees would consume scarce groundwater, while others doubted whether satellite images could capture meaningful ecological change. Now, decades later, NASA’s satellite observations provide compelling evidence that the Great Green Wall is having a measurable and positive impact. According to satellite data, vegetation cover across northern China has increased significantly. Areas once dominated by shifting sand dunes now show stable plant growth, reduced soil erosion, and improved land productivity. These changes are not isolated; they span vast regions, indicating that the project is influencing ecosystems on a continental scale. Desert expansion, once advancing at alarming rates, has slowed dramatically in several high-risk zones. One of the most visible benefits has been the reduction in sandstorms. Cities like Beijing, which once endured frequent and severe dust storms originating from nearby deserts, have seen noticeable improvements in air quality. NASA imagery reveals that wind-blown dust has decreased as vegetation acts as a natural barrier, anchoring soil and reducing airborne particles. This has direct public health benefits, lowering respiratory illnesses and improving overall quality of life for millions of residents. Beyond environmental gains, the Great Green Wall is reshaping regional economies. Stabilized land allows farmers to reclaim fields once lost to encroaching deserts. In some areas, agroforestry—combining trees with crops—has created new income streams while maintaining ecological balance. Satellite data shows that these mixed-use landscapes are more resilient to drought and climate extremes than monoculture farming systems. The project has also influenced local climate patterns. Increased vegetation helps regulate surface temperatures and moisture levels. NASA observations indicate slight increases in local rainfall and reductions in surface heat in reforested zones. While these changes may seem modest, over large areas they contribute to more stable weather patterns and reduced vulnerability to climate shocks. However, the success of the Great Green Wall is not uniform. Satellite analysis also reveals areas where tree survival rates are low or where non-native species struggle to adapt. In response, China has adjusted its strategy, shifting from mass tree planting to ecosystem-based restoration. This includes planting native grasses and shrubs, restoring wetlands, and allowing natural regeneration where possible. The evolving approach reflects lessons learned from decades of experimentation. Another key factor behind the project’s effectiveness is long-term commitment. Unlike short-term environmental campaigns, the Great Green Wall spans generations. NASA’s ability to track changes over decades has been crucial in demonstrating progress that would be invisible on shorter timelines. This long-view perspective underscores an important lesson for global climate efforts: meaningful ecological recovery takes time, patience, and sustained investment. Internationally, China’s experience is drawing attention. Countries facing desertification—from parts of Africa to the Middle East and Central Asia—are studying the Great Green Wall as a model. NASA’s confirmation adds scientific credibility, showing that large-scale land restoration can work when supported by data, adaptive management, and local participation. Still, challenges remain. Climate change continues to intensify droughts, heatwaves, and extreme weather events, threatening fragile restored ecosystems. Experts caution that the Great Green Wall is not a permanent solution but a dynamic system that requires continuous monitoring, maintenance, and adaptation. Satellite technology will remain essential in identifying stress points and guiding future interventions. In the end, NASA’s findings do more than validate a single project—they reshape how we think about humanity’s relationship with nature. The Great Green Wall demonstrates that environmental degradation is not always irreversible. With science, long-term planning, and political will, even vast deserts can be slowed, reshaped, and partially healed. As the world searches for solutions to climate change and land degradation, China’s Great Green Wall stands as a powerful example: proof that large-scale environmental action, guided by data from space, can transform landscapes on Earth.

By Fiaz Ahmed 3 days ago in Earth

Miss Persephone's Manual to a Seemingly Ordinary Life

Miss Persephone was found at the dining table, her blue eyes swollen, her tears arriving and retreating like the tides of the ocean. Earlier that day, her family had visited her in the retirement home where she had lived for eight years. It was her eightieth birthday.

By Imola Tóth4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.