France Aviation Market Size and Forecast 2025–2033

Steady Growth Backed by Aerospace Leadership, Tourism Strength, and Sustainable Innovation

France Aviation Market Overview

The France Aviation Market continues to play a pivotal role in Europe’s air transport and aerospace ecosystem. According to Renub Research, the market is expected to grow from US$ 6.23 billion in 2024 to US$ 7.47 billion by 2033, registering a compound annual growth rate (CAGR) of 2.04% from 2025 to 2033. While growth remains moderate compared to emerging markets, France’s aviation sector benefits from long-term structural strengths such as world-class aircraft manufacturing, a mature airline industry, strong tourism inflows, and sustained government support for aerospace innovation.

France consistently ranks among the most visited countries globally, welcoming millions of international tourists each year. This steady influx of travelers, combined with robust domestic mobility and business travel, continues to underpin demand for air passenger services. At the same time, freight aviation plays a strategic role in supporting high-value exports, industrial supply chains, and global trade connectivity.

The French aviation sector is not only about airline operations. It represents a comprehensive ecosystem encompassing aircraft manufacturing, maintenance and repair operations (MRO), airport infrastructure, defense aviation, and research-driven aerospace technologies. This integrated structure enables France to remain competitive despite rising operational costs and increasingly strict environmental regulations.

France Aviation Industry Landscape

France is globally recognized as one of the leading aviation and aerospace nations. The country has built its reputation through decades of technological excellence, skilled labor, and sustained public-private collaboration. Its aviation footprint spans commercial airlines, military aviation, business jets, helicopters, and advanced aerospace research.

A major pillar of this ecosystem is Airbus SE, headquartered in France and widely regarded as one of the world’s largest aircraft manufacturers. Airbus plays a central role in shaping France’s aviation market by driving innovation in fuel-efficient aircraft, next-generation materials, and sustainable aviation technologies.

France also benefits from a dense airport network, with more than 460 airports supporting domestic, regional, and international connectivity. Paris Charles de Gaulle Airport stands among Europe’s busiest aviation hubs, serving as a critical gateway for both passenger and cargo traffic. Alongside Paris Orly, regional airports such as Lyon, Nice, and Marseille are expanding capacity to support tourism and business travel.

In recent years, the aviation industry has undergone a significant transformation. Airlines operating in France are modernizing fleets, investing in digital solutions, and aligning operations with Europe’s sustainability goals. Beyond commercial aviation, France maintains a strong presence in military and defense aviation, reinforcing its strategic importance within NATO and the broader European defense framework.

Key Factors Driving Growth in the France Aviation Market

Strong Aerospace Manufacturing Base

France’s aviation market is fundamentally supported by its globally competitive aerospace manufacturing industry. The presence of Airbus, along with a broad network of suppliers and engineering firms, strengthens the country’s position as a leading exporter of commercial and military aircraft. Continuous advancements in aerodynamics, avionics, lightweight materials, and engine efficiency contribute to long-term demand for French-designed aircraft.

Government-backed research programs and European Union initiatives further enhance France’s aerospace capabilities. These efforts ensure steady innovation while supporting employment, exports, and technological leadership across the aviation value chain.

Government Support and Strategic Policy Framework

Public policy remains a critical growth enabler for France’s aviation sector. National initiatives such as France 2030 and long-term aerospace roadmaps prioritize sustainable mobility, hydrogen-powered aircraft, and low-carbon aviation solutions. These programs provide financial incentives, research funding, and regulatory clarity to aircraft manufacturers, airlines, and technology providers.

The government also supports airport modernization and digital air traffic management systems, improving efficiency and safety. Through a combination of grants, tax incentives, and public-private partnerships, France continues to position aviation as a strategic industry essential to economic resilience and technological sovereignty.

Rising Passenger Traffic and Tourism Demand

Tourism remains one of the strongest demand drivers for aviation in France. As a cultural, culinary, and business destination, the country attracts leisure travelers year-round while also serving as a key transit hub within Europe. Domestic air travel complements high-speed rail networks by serving longer distances and international connections.

Low-cost carriers and full-service airlines are expanding route networks to meet evolving travel preferences. Airport infrastructure upgrades, smart passenger processing systems, and improved multimodal connectivity further enhance the passenger experience, reinforcing long-term demand growth.

Growth of Air Freight and Logistics

While passenger aviation dominates market revenues, freight aviation plays a crucial supporting role. France’s strong manufacturing, pharmaceutical, and luxury goods sectors rely on efficient air cargo networks to reach global markets. The expansion of e-commerce and time-sensitive logistics has also increased demand for reliable air freight services.

Cargo capacity at major airports continues to expand, supported by investments in digital tracking, cold-chain infrastructure, and automation. These developments strengthen France’s position as a European logistics hub.

Challenges Facing the France Aviation Market

Environmental Regulations and Sustainability Pressures

One of the most significant challenges facing the French aviation industry is compliance with strict environmental regulations. France has implemented ambitious carbon-reduction targets aligned with broader EU climate objectives. Measures such as restrictions on short-haul domestic flights where rail alternatives exist directly impact airline route planning and revenue streams.

Transitioning to sustainable aviation fuels (SAF), hydrogen propulsion, and low-emission technologies requires substantial capital investment and long development timelines. While these initiatives support long-term sustainability, they increase short-term operational costs and financial pressure, particularly for smaller carriers.

High Operating and Labor Costs

France’s aviation sector also contends with high labor and operational expenses. Strong labor unions, regulated wage structures, and frequent industrial actions can disrupt airline operations and reduce efficiency. Airport fees, maintenance costs, and fuel price volatility further challenge profitability.

For low-cost carriers and new entrants, navigating this high-cost environment can be particularly difficult. Balancing workforce stability, sustainability investments, and competitive pricing remains a key strategic challenge for industry participants.

France Aviation Market Segmentation

By Type

General Aviation

Commercial Aviation

Military Aviation

By Revenue Stream

Passenger

Freight

Commercial aviation accounts for the largest share of market revenue, driven by passenger travel and tourism. However, military aviation remains strategically important, supported by defense spending and export demand for advanced aircraft and systems.

Competitive Landscape and Company Analysis

The France aviation market features a mix of global aerospace leaders and specialized aircraft manufacturers. Key companies operating in the market include:

Airbus SE

Bombardier Inc.

Dassault Aviation

Embraer

Leonardo S.p.A.

Pilatus Aircraft Ltd

Robinson Helicopter Company Inc.

Textron Inc.

The Boeing Company

These companies compete across commercial, military, and general aviation segments. Strategic partnerships, technology innovation, and long-term aircraft programs define the competitive dynamics of the market.

Future Outlook: France Aviation Market 2025–2033

Looking ahead, the France aviation market is expected to maintain steady growth through 2033. While short-term challenges such as environmental compliance and cost pressures remain, long-term fundamentals are strong. Continued investment in sustainable aviation technologies, airport modernization, and aerospace R&D will shape the next phase of industry evolution.

France’s leadership in hydrogen-powered aircraft, sustainable fuels, and digital aviation solutions positions the country as a key contributor to the future of global air transport. As international travel stabilizes and sustainability transitions accelerate, the aviation sector will remain an essential pillar of France’s economy and technological leadership.

Final Thoughts

The France Aviation Market, projected to reach US$ 7.47 billion by 2033, reflects a mature yet resilient industry built on innovation, global connectivity, and aerospace excellence. Supported by a strong manufacturing base, robust tourism demand, and proactive government policies, France continues to hold a strategic position within the global aviation ecosystem.

While environmental regulations and high operating costs pose challenges, they also accelerate innovation and long-term competitiveness. For investors, policymakers, and industry stakeholders, France’s aviation sector represents a stable market with sustained relevance in the global transition toward smarter and more sustainable air transport.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in 01 and other communities.

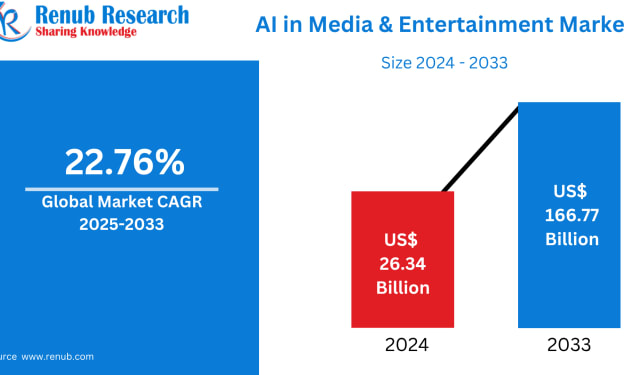

Global AI in Media & Entertainment Market Size & Forecast 2025–2033

Market Snapshot: A Decade of Explosive Growth The Global AI in Media & Entertainment Market is entering a transformative growth phase. According to Renub Research, the market is projected to surge from US$ 26.34 billion in 2024 to an impressive US$ 166.77 billion by 2033, registering a robust CAGR of 22.76% from 2025 to 2033.

By Aaina Oberoi12 days ago in 01

World Leaders React After U.S. Strikes Spark Global Concern

World leaders are reacting to overnight strikes by the U.S. that have altered the global scenario. Countries are currently holding debates regarding what this development implies for global peace and future global policies by the U.S. based on international law.

By iftikhar Ahmad7 days ago in 01

Best Companies Building Next-Gen Hotel Booking Apps in 2026

The travel and hospitality industry continues to evolve rapidly, and hotel booking apps have become a central part of how travelers plan and manage their stays. In 2026, users expect more than just room listings and prices—they want personalized recommendations, real-time availability, seamless payments, and smooth user experiences across devices. To meet these expectations, businesses are partnering with experienced development companies capable of building next-generation hotel booking apps that are innovative, secure, and scalable.

By shane cornerus5 days ago in 01

A Failed Artist, A Disillusioned Poet, An Underpaid Game Show Host

I took my son and niece to Gori, a small town in Georgia where Joseph Stalin was born. They talked me into visiting the Stalin's Museum, the largest in the post-Soviet space. I had resisted going there because I just can't stand the monster and know enough about him, or so I thought.

By Lana V Lynx5 days ago in FYI

Comments

There are no comments for this story

Be the first to respond and start the conversation.